Start Me Up: Growth Time for Private Wealth and Private Markets

By Samuel Dale, Managing Editor of Private Markets, With Intelligence

Wealth managers represent the fastest growing investor group in private markets. Boston Consulting Group estimates there could be $3 trillion more invested in private markets from wealth managers by 2030, for a total of $5.8 trillion.

The opportunities for diversification and growth across different asset classes are plentiful.

The benefits flow both ways with new assets classes available for wealth management clients and an enormous new investor base for fund managers.

Some suggest private markets still requires a game-changing product to open up the space to all investors.

For example, the creation of the index tracker by Vanguard’s Jack Bogle in the early 1980s transformed low-cost passive public markets investing over the following decades.

The reality is that demand is driving significant innovation right now with a plethora of evergreen offerings with more liquidity and transparency than ever before.

Each private markets asset class is seeing money flow into the evergreen structures best suited to their underlying assets.

We are yet in the early stages of private wealth investing in private markets products, and fund managers are still transforming their offerings for new investors. There will be much more change to come from market participants and regulators.

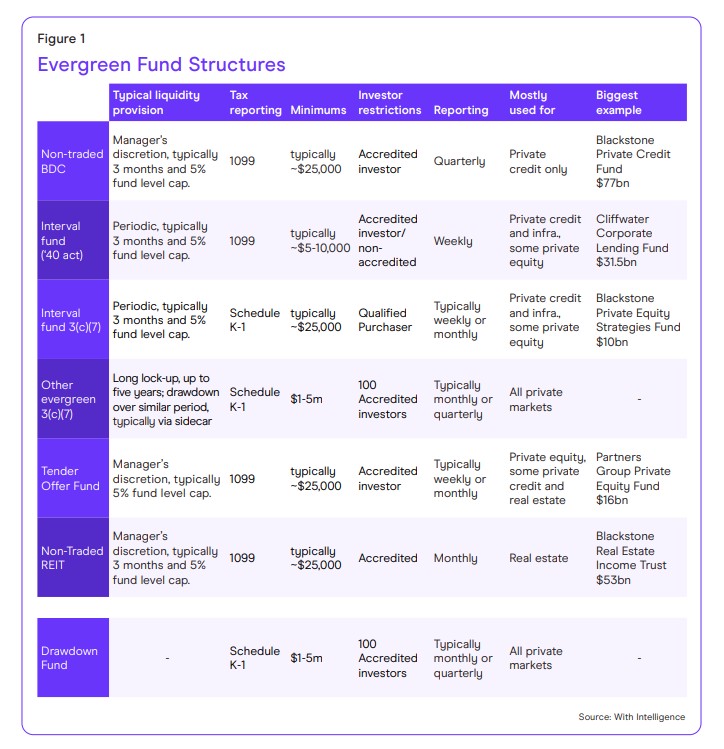

Private Credit

Private credit has been the most popular sector for accredited investors in recent years with a variety of structures used.

There are a variety of publicly traded private credit ETFs, which offer a way to gain exposure. There are also publicly listed, private or non-traded business development companies; interval funds; tender offer funds; listed closed-end funds; and evergreen or closed-ended 3(c)(7) funds.

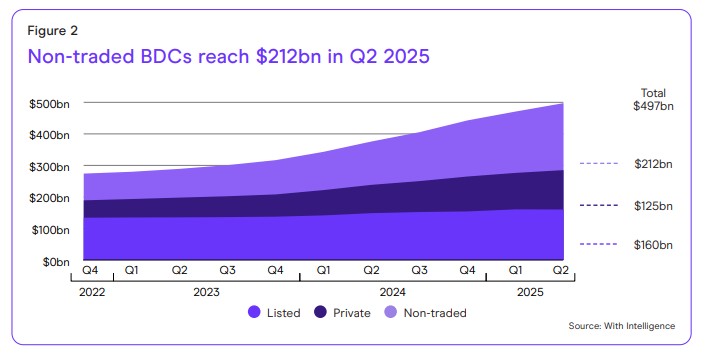

For accredited investors, non-traded BDCs have proven the most popular structure due to transparency, favorable tax treatment, and their focus on U.S. middle-market loans.

Non-traded BDCs have taken up a growing share of wealth manager capital in private credit. They are set to hold $200 billion in private credit assets this year and on course to hit $1 trillion by 2030, based on the post-2022 growth rate (CAGR: 39%).

While most assets have been focused on direct lending, there is a growing appetite among wealth managers to invest in specialty finance, especially asset-backed lending; and more opportunistic and distressed assets too.

We would expect investor interest to grow in these areas as private wealth investing grows and matures, as well as rising concerns over pricing in U.S. middle marketing lending.

Private Equity

Private equity evergreen products have grown less sharply than private credit with sector focus on secondaries.

Interval funds have proven most popular due to more flexible distributions and better liquidity matching for private equity.

With Intelligence estimates that the top 15 interval funds have added $60 billion in the last five years.

Partners Group Private Equity Group, which launched in 2001 as the first interval fund in private equity, added $9.8 billion in the last five years. It is by far the largest fund with $16.6 billion in assets.

Real Estate

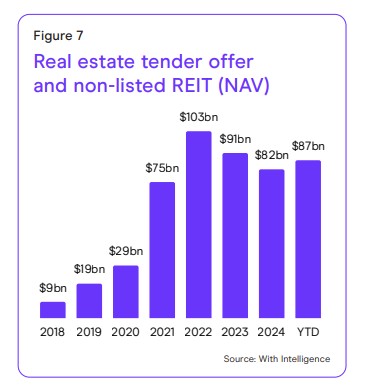

Real estate has struggled significantly since the impact of COVID-19, and its aftershocks, on commercial real estate assets.

Redemption requests hit most non-traded real estate investment trusts from 2022, most notably Blackstone’s market-leading $53 billion fund by assets under management. The investment giant successfully managed the queue and has even added assets.

Redemption queues have nearly halved after $56 billion was withdrawn overall, although some pockets remain such as $1 billion waiting to be pulled out of Starwood Real Estate Income Trust.

Inflows have begun to flow again from wealth managers across interval funds and non-traded REITs from the 2024 lows.

A key driver has been the move from lifecycle REITs to net asset value REITs. This is boosting transparency on NAV through monthly appraisals and providing greater liquidity via redemptions of 2% of aggregate NAV per month and 5% per quarter, while still outperforming public REITs.

Infrastructure

Infrastructure assets have proven a popular addition to wealth management portfolios in recent years, especially as a replacement for fixed income assets.

With Intelligence has tracked 14 infrastructure fund launches targeting private wealth assets since 2024.

Investment consulting and outsourced chief investment officer firms have led the recent launch charge, with Stepstone Group, Hamilton Lane, Meketa, Russell Investments, GCM Grosvenor and Wilshire.

As well as replacing fixed income and diversifying portfolios, some thematic funds such as energy transition have proven attractive.

Macquarie Asset Management’s Energy Transition Infrastructure Fund, at close to $500 million AUM is targeting $1 billion over the next 12 months.

Trust and Education

The biggest challenge for private wealth investing is educating clients about how best to utilize products, as well as gaining trust from asset managers.

The apparent liquidity mismatch between assets and redemption terms can still leave clients fearful about how to exit and when.

Blackstone’s high profile REIT redemption queue in 2022 caused initial concern but is now seen as an example of successful handling of concerns, even among rivals.

Big name players have a big role to play in gaining that trust.

Today, clients understand seemingly simple products such as ETFs or fixed-rate mortgages that conceal more complex underpinnings.

The aim for private markets is to get to stage where clients are as comfortable investing through its products. Fund managers and private clients are moving that way, and the opportunities for all are enormous.

Sam Dale is managing editor of private markets at With Intelligence, a provider of investment intelligence for allocating decisions, fundraising, and business development. Over more than 10 years at With Intelligence, he has held events, research, and editorial roles across hedge funds and private markets in London and New York. He previously spent five years covering U.K. wealth management in London. Today, he leads editorial and research across private equity, private credit, infrastructure, and real estate.

The views and opinions expressed in the preceding article are those of the author and do not necessarily reflect the views of AltsWire.

Click here to visit the AltsWire directory page.