Pragmatism Prevails in Oil and Gas as 2025 Market Reset Shapes 2026 Outlook

By Brad Updike, Attorney, Mick Law P.C. LLO

If 2025 proved anything for the oil and gas industry, it was that pragmatism – grounded in physics, economics, and politics – has reclaimed the driver’s seat.

With a few twists and turns ahead, the market reset that began roughly a year ago appears poised to extend into 2026.

While global supply and demand dynamics suggest oil prices are likely to trend lower this year, projected between $55 and $65 per barrel of crude oil, many upstream companies are quietly breathing a sigh of relief.

For upstream companies with scale and sizable exploration, development and production (E&P) budgets, recent U.S. energy policy changes are increasingly viewed as a long-overdue course correction rather than a headwind. Infrastructure development, regulatory clarity, and a renewed focus on energy security are increasingly seen as worth the near-term pressure on crude prices. Though President Trump’s policies have contributed to softer pricing today, the more informed E&P pragmatists view this as a necessary trade-off that will help bolster oil, natural gas, and natural gas liquids economics beyond 2026.

Recent commentary from RBN Energy LLC, a leading analytics and data company for the energy industry, reinforces the importance of nuance over headlines. RBN’s January 2026 outlook urged investors to “follow the molecules” – tracking how hydrocarbons actually move through markets and hubs rather than relying on oversimplified narratives. From Mick Law’s perspective, RBN’s favored prognostications for 2026 include:

- In the Permian Basin, natural gas prices are likely to remain under pressure through much of 2026. Production continues to outpace takeaway capacity, keeping prices at the Waha Hub historically depressed. Waha Hub prices fell below $0 a total of 49 times in 2024 and averaged just $0.77 per 1,000 cubic feet (MCF) of natural gas that year, compared with $1.96 per MCF in 2025. Relief, however, is finally on the horizon. Two greenfield pipelines and one brownfield expansion project are expected to come online in 2026, adding approximately 4.5 billion cubic feet (BCF) per day of egress capacity and helping to rebalance the basin.

- More natural gas liquids production growth is coming. Over the past decade, U.S. natural gas liquids production grew at a 7.6% compound annual rate – more than double that of oil and natural gas. The addition of new Permian pipelines in 2026, along with stabilized and higher natural gas prices driven by consumption growth, is expected to support stronger natural gas liquids fundamentals in the coming years.

- While artificial intelligence, liquefied natural gas, and data centers are still expected to increase U.S. natural gas demand in the coming years, some of the anticipated AI-driven power growth may be supplied by alternative energy sources, potentially limiting the overall impact on natural gas consumption.

- Operational efficiency remains another defining theme. Despite an 8% average annual decline (2002-2025) in U.S. oil rig counts, production has climbed from 12 million barrels per day in 2022 to nearly 13.8 million barrels per day – even though the U.S. rig count stands at 400 today versus 575 in 2022. Advances in automation, pad drilling, completions, and geo-steering continue to drive higher output per rig and support capital discipline heading into 2026 and 2027.

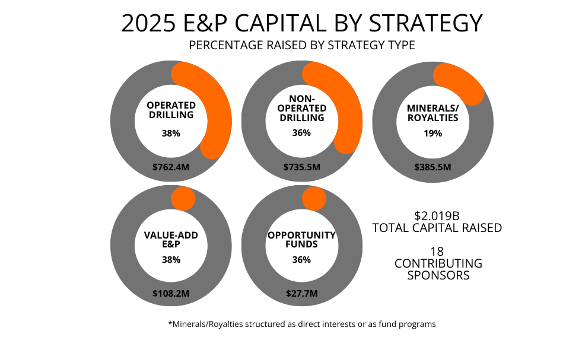

In the world of alternative investments, retail capital trends reflect this renewed confidence. In 2025, 18 upstream sponsors covered by Mick Law raised approximately $2.02 billion across 38 private oil and gas programs. This represents more than a 40% increase year over year and the highest capital raise year we’ve ever tracked. The majority of this capital will fund operated and non-operated drilling, with a notable resurgence in value-added E&P and royalty programs. There were six top sponsors, ranked by capital raise:

- U.S. Energy Development Corp.: $847.8 million;

- MDS Energy: $259.3 million;

- WhiteHawk Income Corp.: $258.2 million;

- Mewbourne Development Corporation: $180 million;

- Montego Energy Partners: $108.2 million; and

- Renaissance Growth Partners: $97 million.

The funded capital within the programs Mick Law reviewed varied, with several sponsors funding their initial retail programs in 2025. This included Trellis Energy Partners, Mountain V Oil & Gas, and Citizen Energy Ventures. Resource Royalty and Purified Resource Partners both raised capital for non-operated acquisitions toward the end of 2025.

It should be an interesting time for the oil and gas investment sponsors we review in 2026 and 2027, with natural gas markets presently expecting upside. Lower oil prices, easing cost inflation, and improving natural gas fundamentals are converging to create opportunity, provided underwriting discipline remains front and center. In a market still prone to volatility, cautious independent underwriting by a firm with petroleum engineers evaluating a program’s mineral value, costs, risks, and structure will be more important than ever.

Brad Updike, an attorney and director at Mick Law P.C. LLO, manages the firm’s energy and tax-oriented practice. He joined the firm in August 2006, and his areas of practice include securities law, oil and gas, private equity, conservation real estate, DPP due diligence, taxation analysis relating to securitized financing, and securities advertising practices. On a local level, Updike has also served the legal needs of Omaha-based clients on matters relating to estate planning, private placements, trademark law, and 501(c)(3) non-profit taxation matters. Prior to joining Mick Law, Updike worked as an attorney at Securities America Inc., or SAI.

The views and opinions expressed in the preceding article are those of the author and do not necessarily reflect the views of AltsWire.

For more Mick Law news, please visit their directory page.