Alts Fundraising Hits $75B Through May as BDC Capital Formation Declines 55% Year-Over-Year

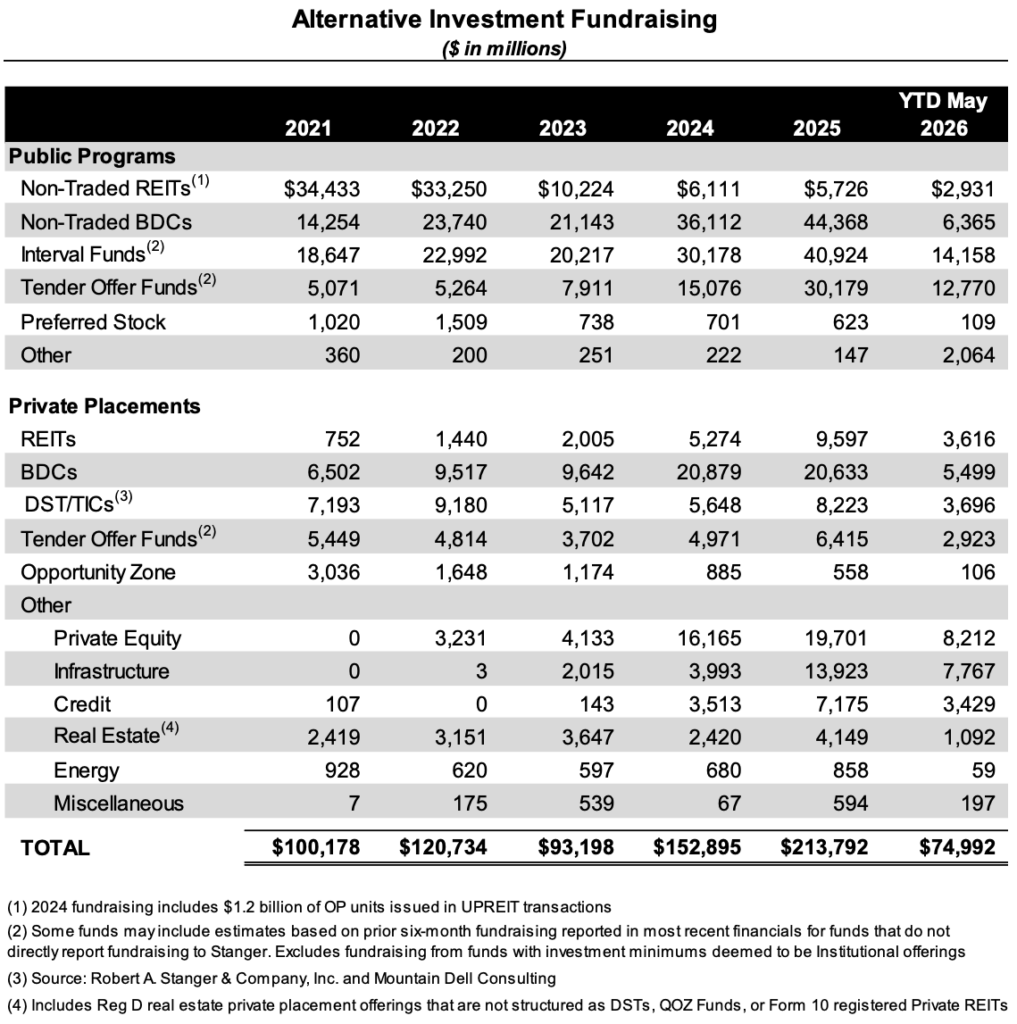

Through the first five months of 2026, alternative investment fundraising totaled approximately $75 billion, down 9% from $82.8 billion in the same period of 2025, according to the latest analysis from investment banking firm Robert A. Stanger & Co. The decline was concentrated primarily among nontraded business development companies and credit-oriented strategies.

Combined publicly registered and private placement BDC fundraising totaled approximately $11.9 billion through May 2026, down 55% year-over-year. Based on the most recent reporting, combined BDC redemptions totaled approximately $12.9 billion over the same period, resulting in net outflows of approximately $1 billion. Across all credit strategies, year-to-date fundraising totaled approximately $27.9 billion, down 37% year-over-year.

“Through five months, 2026 has been defined by a clear rotation out of credit,” said Kevin T. Gannon, chairman and chief executive officer of Stanger. “BDC fundraising is down more than 50% year-to-date, and credit’s share of the market has fallen from more than half to roughly a third.”

HALO strategies, hard assets with low obsolescence, continued to show relative strength. Combined real estate and infrastructure fundraising reached approximately $23.1 billion through the first five months of 2026, up 33% from the same period in 2025. Infrastructure strategies led that growth, rising 61% year-over-year, a figure that includes the recent Blackstone Digital Infrastructure Trust (NYSE: BXDC) public offering, while real estate strategies increased 12%.

May’s fundraising data includes Blackstone’s initial public offering of BXDC, an externally managed blind-pool real estate investment trust focused on data centers net-leased to hyperscalers. While BXDC is not structured as a traditional nontraded net asset value REIT, it pairs exposure to a private real estate sector with public-market liquidity, external management by an alternative investment sponsor, and a fee structure that Stanger previously estimated to be approximately 44% lower than the conventional NAV REIT structure.

Year-to-date gross fundraising by product category through May 2026, compared with prior years, is summarized in the following table.

“Investors are not leaving alternatives; they are becoming more selective about where they want exposure, and the data increasingly points toward hard assets with durable demand drivers,” said Gannon.

“BXDC is an important development as it pairs exposure to one of the most sought-after sectors in real estate today with a structure designed to address two of the biggest investor priorities: liquidity and fees. If the vehicle gains traction, other sponsors will take note, and the next phase of capital formation may be defined by sponsors that can pair high-demand hard asset exposure with product structures that deliver better access, liquidity, and value,” Gannon added.

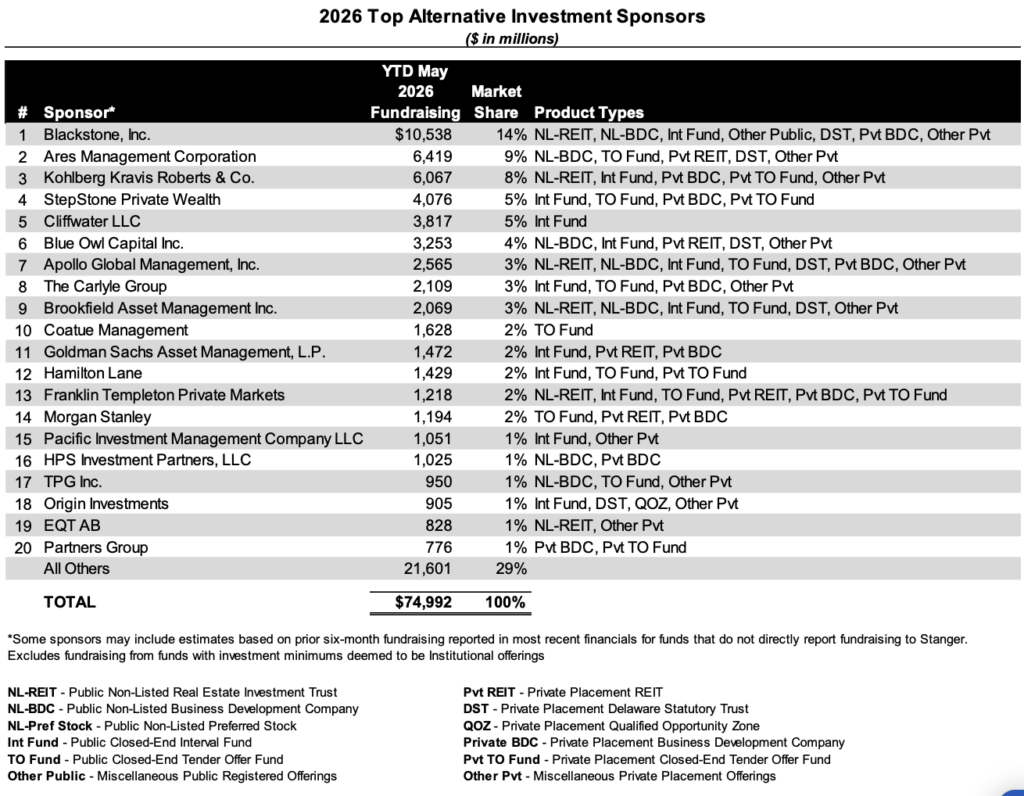

The top 20 sponsors by year-to-date gross fundraising are shown below. The top five are Blackstone (14% of market share), Ares Management Corporation (9%), KKR & Co. (8%), StepStone Private Wealth (5%), and Cliffwater (5%).

Founded in 1978, Robert A. Stanger & Co. is an investment banking firm providing advisory, valuation, and capital markets services to real estate investment trusts, partnerships, and related entities.

Visit the AltsWire directory page.