AI Disruption Risk Concentrated in Non-Traded BDC Portfolios, Stanger Says

As public markets increasingly price in the risks and disruptions of artificial intelligence, new industries are coming into focus. Against this backdrop, investment banking firm Robert A. Stanger & Company Inc. has released an AI Disruption Risk Assessment of the publicly registered, non-traded business development company landscape.

The firm said it considers this analysis essential following recent volatility and AI-driven repricing across public credit and equity markets. The assessment evaluates how AI advancements may influence underlying sector exposure within the non-traded BDC sector.

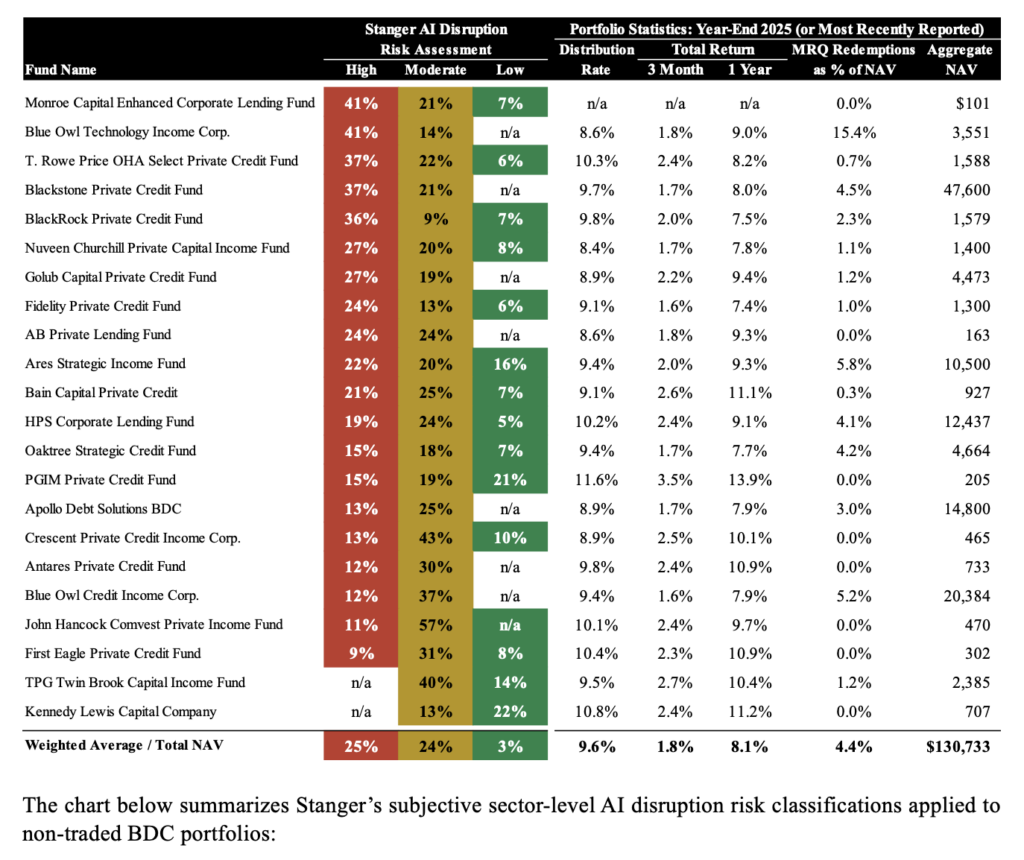

The assessment applied an AI disruption risk profile to each BDC’s most recently disclosed top five sector exposures, evaluating workforce displacement risk, margin compression potential, business-model vulnerability, and barriers to AI adoption. Across the universe analyzed, the top five sector exposures represent, on average, 52% of total portfolio allocation, underscoring concentration risk embedded in non-traded BDC portfolios.

In aggregate, the analysis covers 22 non-traded, net asset value BDCs representing $235.2 billion in total investment value and $130.7 billion in total net asset value, providing a comprehensive view of how AI-related disruption may impact credit risk and portfolio valuations across the space.

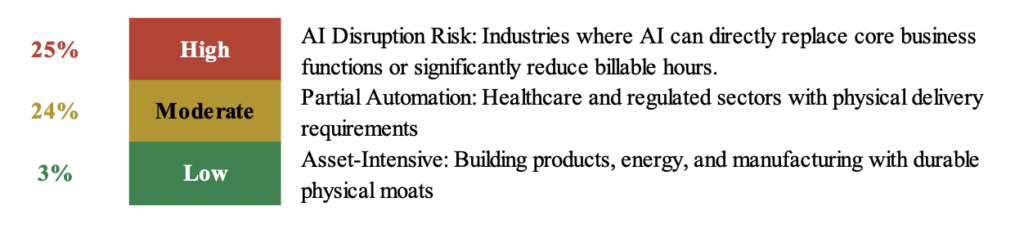

Aggregate Portfolio Risk Profile

The aggregate portfolio exposure across the 22 non-traded BDCs reviewed shows a meaningful concentration in the top five reported sectors vulnerable to artificial intelligence disruption.

“These findings suggest that AI disruption is not a theoretical or long-dated risk for BDC investors. Artificial intelligence is already reshaping cost structures, competitive dynamics, and credit fundamentals in many of the sectors where non-traded BDCs are most active. Investors and advisers need to understand that not all sector exposure is created equal in an AI-driven economy.” said Kevin T. Gannon, chairman and chief executive officer of Robert A. Stanger & Co.

“These findings suggest that AI disruption is not a theoretical or long-dated risk for BDC investors. Artificial intelligence is already reshaping cost structures, competitive dynamics, and credit fundamentals in many of the sectors where non-traded BDCs are most active. Investors and advisers need to understand that not all sector exposure is created equal in an AI-driven economy.” said Kevin T. Gannon, chairman and chief executive officer of Robert A. Stanger & Co.

Stanger’s analysis shows that software, business services, and financial services represent the largest concentration of high-risk exposure across the non-traded BDC universe. These sectors are already experiencing rapid AI adoption that may compress margins, displace labor-intensive workflows, and alter traditional business models, all factors that may have downstream implications for credit performance.

Healthcare-related sectors generally fall into the medium-risk category, benefiting from regulatory oversight and the physical nature of care delivery, but remain exposed to AI-driven disruption in diagnostics, administration, and data-intensive services. In contrast, sectors such as building products, chemicals, food manufacturing, and energy exhibit lower near-term disruption risk due to tangible asset intensity and operational complexity.

“When we mapped individual BDC portfolios to our AI risk framework, the degree of concentration in high-disruption sectors was striking and echoes what is occurring in the public markets,” said Michael S. Covello, executive managing director at Robert A. Stanger & Co. “Middle-market companies, the core borrowers for BDCs, often lack the capital and organizational flexibility to adapt as quickly as larger enterprises. That reality makes AI exposure an increasingly important credit variable that traditional underwriting models may not fully capture – a gap that, ironically, AI-powered tools are now helping to close.”

The analysis highlights several important implications for investors and financial advisers evaluating non-traded BDCs. A substantial portion of the top five sectors face elevated levels of AI-driven disruption, warranting additional scrutiny. At the same time, AI exposure varies materially by manager, creating meaningful differentiation across the non-traded BDC landscape that may not be readily apparent through conventional metrics alone. As a result, AI disruption risk should be incorporated into the due diligence process, alongside established considerations such as NAV stability, leverage, portfolio diversification, and distribution sustainability.

“This assessment involves subjective classifications of sectors by Stanger. Not all companies within higher-risk sectors will be negatively impacted by AI, and some may in fact benefit from it. We encourage sponsors to enhance disclosure and provide more granular portfolio information, valuation metrics, credit performance and non-accrual trends to further support informed due diligence.” said Raghav Devalla, associate at Robert A. Stanger & Co.

The assessment is sorted by high-risk exposure in descending order. Each percentage reflects the combined disclosed sector exposures of the BDCs analyzed, aggregated, and classified by Stanger.

The four BDCs with the highest percentage of high-risk exposure are: Monroe Capital Enhanced Corporate Lending Fund; Blue Owl Technology Income Corp.; T. Rowe Price OHA Select Private Credit Fund; and Blackstone Private Credit Fund, or BCRED. These first two each report 41% high-risk exposure, and the latter two report 37% high-risk exposure.

Blackstone’s BCRED recently provided insight into how AI is influencing its investment strategy. The firm emphasized a bifurcated view of the market, distinguishing between companies positioned to thrive and those vulnerable to disruption.

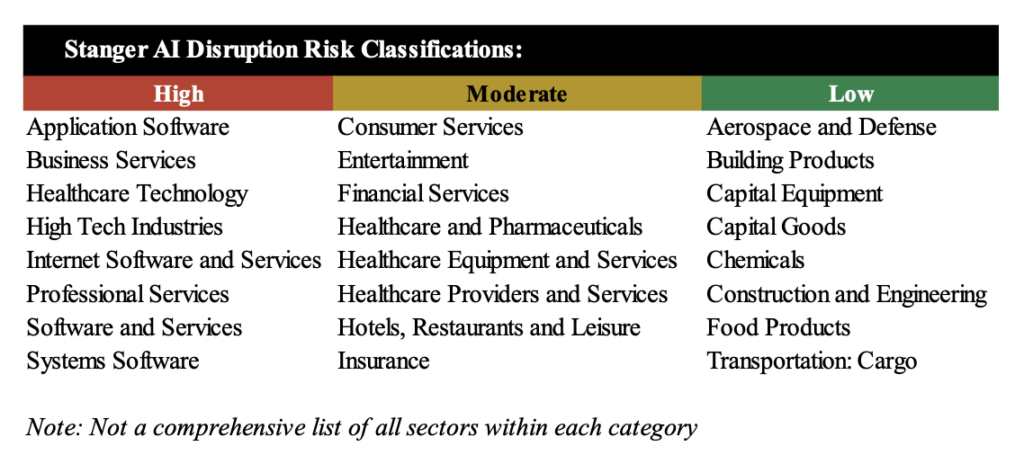

The chart below summarizes Stanger’s subjective sector-level AI disruption risk classifications applied to non-traded BDC portfolios.

Source: Robert A. Stanger & Co. Inc. Sector allocations based on each fund’s disclosed top five industry concentrations.

Founded in 1978, Robert A. Stanger & Company is an investment banking firm specializing in providing investment banking, financial advisory, fairness opinion and asset and securities valuation services to partnerships, real estate investment trusts, and real estate advisory and management companies in support of strategic planning and execution, capital formation and financings, mergers, acquisitions, reorganizations, and consolidations.

Click here to visit the AltsWire directory page.