Private Debt’s Inflation Advantage: Why Direct Lending Has Outpaced Bonds on Real Returns

By Joseph DaGrosa Jr., Chairman and CEO, Axxes Capital

Understanding Income Opportunities Across Public and Private Credit Markets

For most of the past decade, investors struggled to find meaningful yield as interest rates remained near historic lows following the Global Financial Crisis. Traditional fixed income portfolios generated modest income while offering limited protection against inflation. That environment changed sharply beginning in 2022 as inflation surged and central banks aggressively raised interest rates.

Today, investors once again have meaningful choices in fixed income markets. Higher rates can now be found across both public and private credit markets, ranging from short-term Treasury bills to investment-grade corporate bonds, high yield debt, leveraged loans and private market direct lending strategies.

While public markets generally provide greater liquidity and transparency, private markets often provide higher yields in exchange for reduced liquidity and differing risk profiles. Increasingly, investors are blending both approaches to create diversified income portfolios. Investors can also blend short-term and long-term exposures depending on their views on inflation, interest rates, liquidity, and income stability.

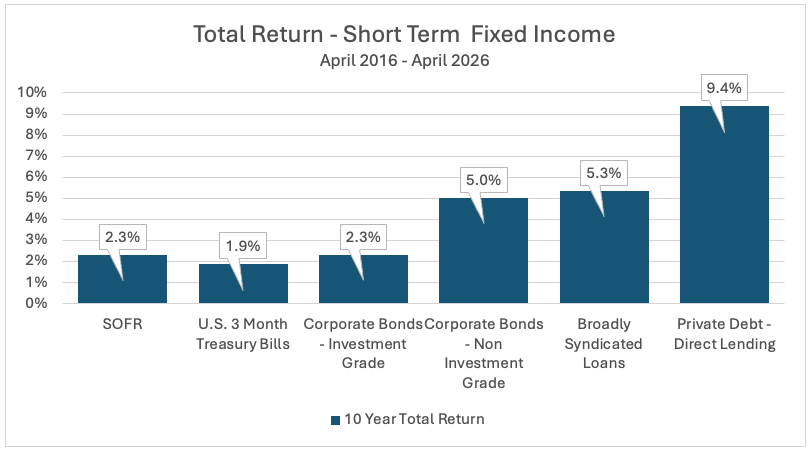

Short-Term Yield Opportunities

Short-duration debt strategies have become increasingly attractive because they generally carry lower interest rate sensitivity while still generating meaningful income. Many short-duration and private debt instruments are tied to floating-rate benchmarks such as secured overnight financing rate, or SOFR, as set by the U.S. Federal Reserve, allowing yields to quickly adjust upward if or as rates rise.

Figure 1: Fact Set for public market instruments (SOFR, U.S. treasury bills, corporate bonds), Morningstar LSTA Index for Broadly Syndicated Loans, Cliffwater Direct Lending Index for private debt direct lending. Total returns as at April 2026, except Cliffwater, December 2025. Performance data shown reflects historical results and does not guarantee future outcomes.

Private debt strategies have historically offered higher yields relative to public credit markets, though future results may differ. These strategies typically lend directly to middle-market companies using floating-rate structures tied to SOFR. As short-term interest rates increased, coupon income on many private loans increased as well. Short-duration fixed income strategies have benefited from lower duration exposure and have generally outperformed longer-term instruments over the last 10-year period.

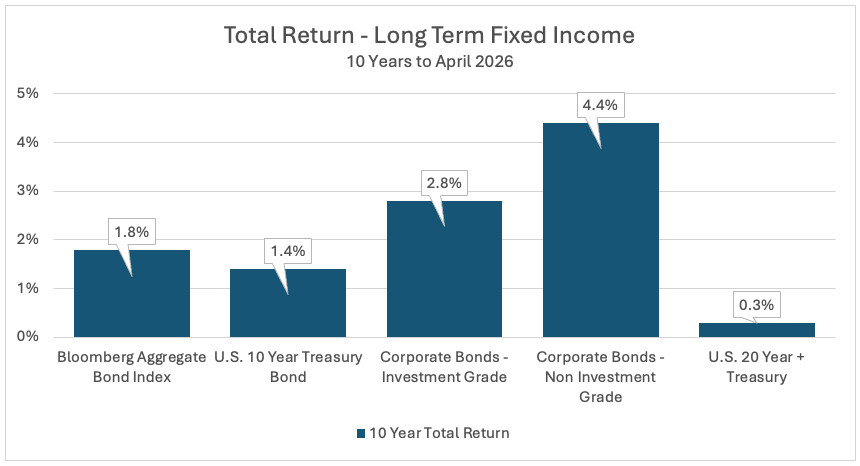

Long-Term Yield Opportunities

Longer-duration bonds continue to play an important role in diversified portfolios, particularly for investors seeking stability, portfolio protection during recessions or long-term liability matching. However, long-duration bonds are significantly more sensitive to inflation and rising interest rates because their coupon payments are fixed for longer periods of time.

Figure 2: Fact set for public market instruments (Bloomberg Aggregate, U.S. treasury bills, corporate bonds). Total returns as of April 2026.

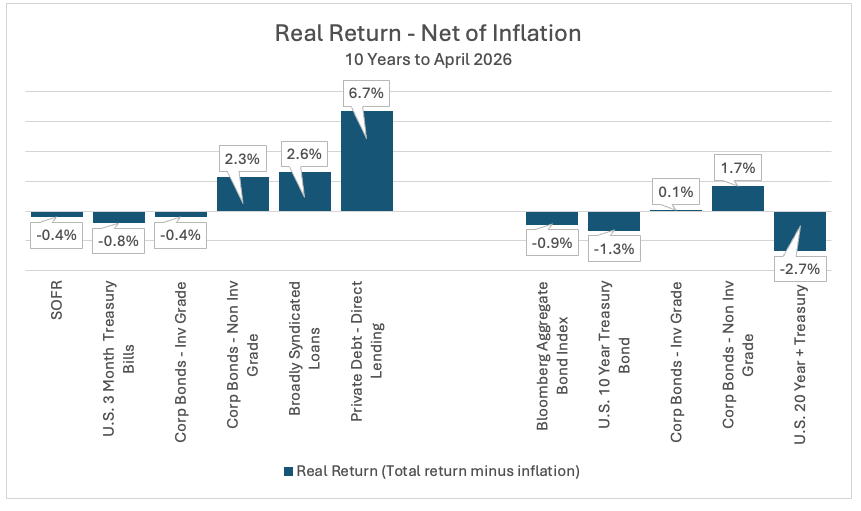

The Ravages of Inflation on Bond Returns

Inflation is one of the greatest long-term risks for fixed income investors because it reduces the purchasing power of future coupon or interest payments. Over the past 10 years, U.S. headline inflation averaged approximately 2.7% annually, according to the U.S. Bureau of Labor in April 2026. For bond investors, this means nominal returns can appear positive while real purchasing power barely improves or worse, actually falls as interest rates fail to keep pace with inflation. As noted below in Figure 3, many public market instruments produced near 0% or negative returns after adjusting for inflation. In contrast, direct lending private debt strategies have returned 6.7% above inflation, delivering the highest real return. Further, the Bloomberg Barclays Aggregate Bond Index is trading at the same level as 2009 after adjusting for inflation, producing a 0% real return over the past 17 years, according to StockCharts in April of this year.

Figure 3: Fact set for public market instruments (SOFR, U.S. treasury bills and bonds, corporate bonds), Morningstar LSTA Index for Broadly Syndicated Loans, Cliffwater Direct Lending Index for private debt direct lending. All figures net of inflation as of April 2026, Cliffwater as of December 2025.

Conclusion: Why Private Debt Has Gained Attention

Many investors are exploring private debt and direct lending strategies because they offer a different return and risk profile versus traditional bonds. The vast majority of private loans are floating rate directly tied to SOFR, are senior and secured sitting at the top of the capital stack. As inflation and interest rates rise, direct lending rates automatically adjust upward. By contrast, long-term fixed-rate bonds may lose value because their coupon payments remain fixed while inflation rises.

Investors must still evaluate key risks associated with private debt such as credit quality, liquidity terms, manager selection, and economic risk. Private investments are generally less liquid than public bonds and are often accessed through structures such as interval funds, tender offer funds, private BDCs, or institutional partnerships. Combined with higher base returns and senior positioning in capital structures, private debt has exhibited strong historical risk-adjusted returns for yield-seeking investors. While private debt may offer higher yields, these strategies involve significant risks, including limited liquidity, higher default risk, valuation uncertainty, and reliance on manager expertise.

Today, U.S. headline inflation is running at 3.8%, excluding the post Covid period, its highest level since 2011. Periods of inflation often prompt investors to evaluate how different income strategies may behave under varying economic conditions. Income generation increasingly requires flexibility across both public and private markets. Investors who combine traditional bonds, short-duration credit, and carefully selected private debt strategies may be better positioned to generate income while managing inflation risk over the long term.

Joseph DaGrosa Jr. is the chairman and chief executive officer of Axxes Capital. He has more than 30 years of experience investing across multiple industries, including insurance, retail, food and beverage, real estate, hospitality, healthcare, aviation, sports and entertainment. DaGrosa also serves as chairman of a private equity firm, DaGrosa Capital Partners LLC, that is focused on making minority investments in companies located throughout the United States, Western Europe, and Latin America.

Axxes Capital is a private markets investment management firm that partners with independent asset managers to offer access to private equity, credit, structured finance, and alternative strategies through adviser-friendly investment vehicles.

The views and opinions expressed in the preceding article are those of the author and do not necessarily reflect the views of AltsWire.

Visit the AltsWire directory page.