Nontraded Closed-End Funds Reach $261B as Private Equity Funds Lead

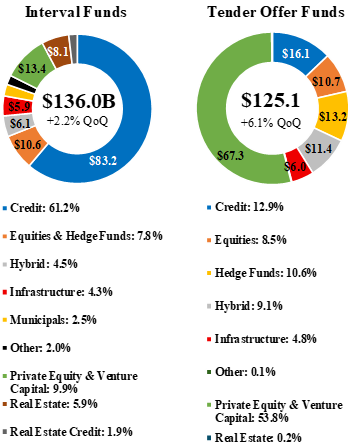

Nontraded closed-end funds reached $261 billion in aggregate net asset value in the second quarter of 2026, a 4% quarter-over-quarter increase. Interval funds accounted for $136 billion, up 2.2% from the prior quarter, while tender offer funds grew 6.1% to $125.1 billion, according to Robert A. Stanger & Co. The investment banking firm now tracks 308 effective closed-end funds, consisting of 173 interval funds and 135 tender offer funds.

Aggregate NAV by investment focus for interval funds and tender offer funds is summarized below.

The newly introduced fund-level redemption data summarizes the most recently reported repurchase activity for the 25 largest credit interval funds by aggregate NAV. Across those funds, net redemptions equaled approximately 5% of the corresponding NAV basis for the most recently reported quarters, compared with 5.4% in immediately preceding quarters. Because funds report on varying schedules, this figure combines Q2 2026 results for six funds and Q1 2026 results for the remaining 19 and should not be interpreted as a single-quarter market total. Based on most recently reported data, these 25 funds have returned nearly $6.4 billion to investors in 2026.

The most notable fund-level result came from Cliffwater Corporate Lending Fund, the largest interval fund by aggregate NAV at more than $30 billion. Based on Stanger estimates, the fund received repurchase requests equal to 17% of NAV in its most recent offer and repurchased 5% of NAV, or $1.6 billion, satisfying approximately 29% of requests. In its prior offer, Cliffwater expanded its standard 5% quarterly offer to 7%, returning $2.3 billion to investors and satisfying roughly half of total requests.

“The private credit liquidity cycle extends beyond [business development companies],” said Kevin T. Gannon, chairman and chief executive officer of Stanger. “Our new interval fund data shows meaningful investor demand for liquidity within credit-focused vehicles, but also substantial variation from fund to fund. Sponsors are continuing to return capital within defined program limits, while proration is occurring where requests exceed those limits. That is how semi-liquid structures are designed to function, and this expanded coverage gives greater visibility into where liquidity demand is concentrated and how individual funds are managing it.”

Gross fundraising across interval and tender offer funds totaled approximately $30.5 billion year-to-date through May 2026, essentially unchanged from $30.6 billion during the same period of 2025. Interval funds raised $14.2 billion through May 2026, with credit strategies contributing $8.4 billion, or 59% of gross sales. Tender offer funds raised $16.3 billion, led by private equity and venture capital strategies, which raised $8.7 billion and accounted for 54% of gross sales.

Private equity and venture capital strategies led interval fund performance across all three trailing periods. Funds in the category represented seven of the top 10 performers over three months and six of the top 10 over both six and 12 months. Interval fund performance leaders across three-month (Pre-IPO & Growth Fund), six-month (ARK Venture Fund), and one-year (ARK Venture Fund) time periods are summarized below.

Founded in 1978, Robert A. Stanger & Co. is an investment banking firm providing advisory, valuation, and capital markets services to real estate investment trusts, partnerships, and related entities.

Visit the AltsWire directory page.