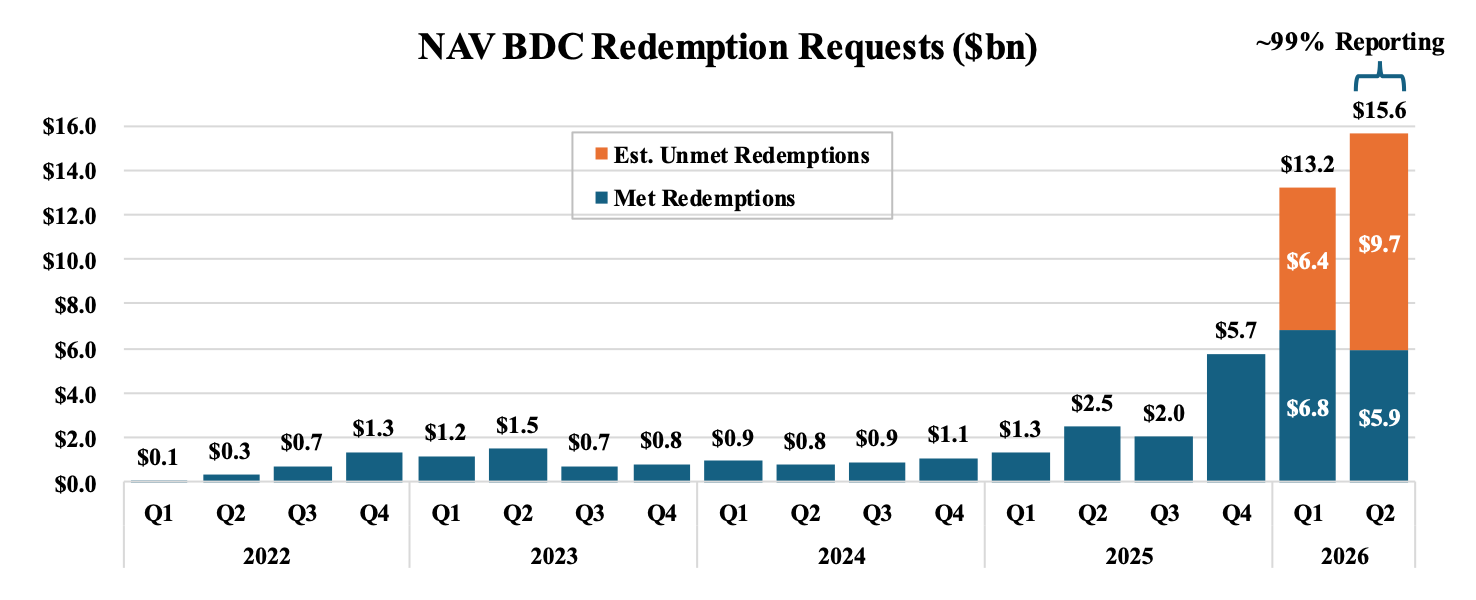

Nontraded BDCs Return Nearly $5.9B to Investors in Q2, More Than $12.7B Year to Date

With approximately 99% of the market reporting, nontraded net asset value business development company sponsors have delivered nearly $5.9 billion in liquidity to investors in the second quarter ended June 30, 2026, which the Robert A. Stanger & Co., Inc., said demonstrates the resilience of the semi-liquid vehicle structure even in the face of historically elevated redemption demand. According to Stanger year-to-date, total redemptions met by NAV BDCs have exceeded $12.7 billion.

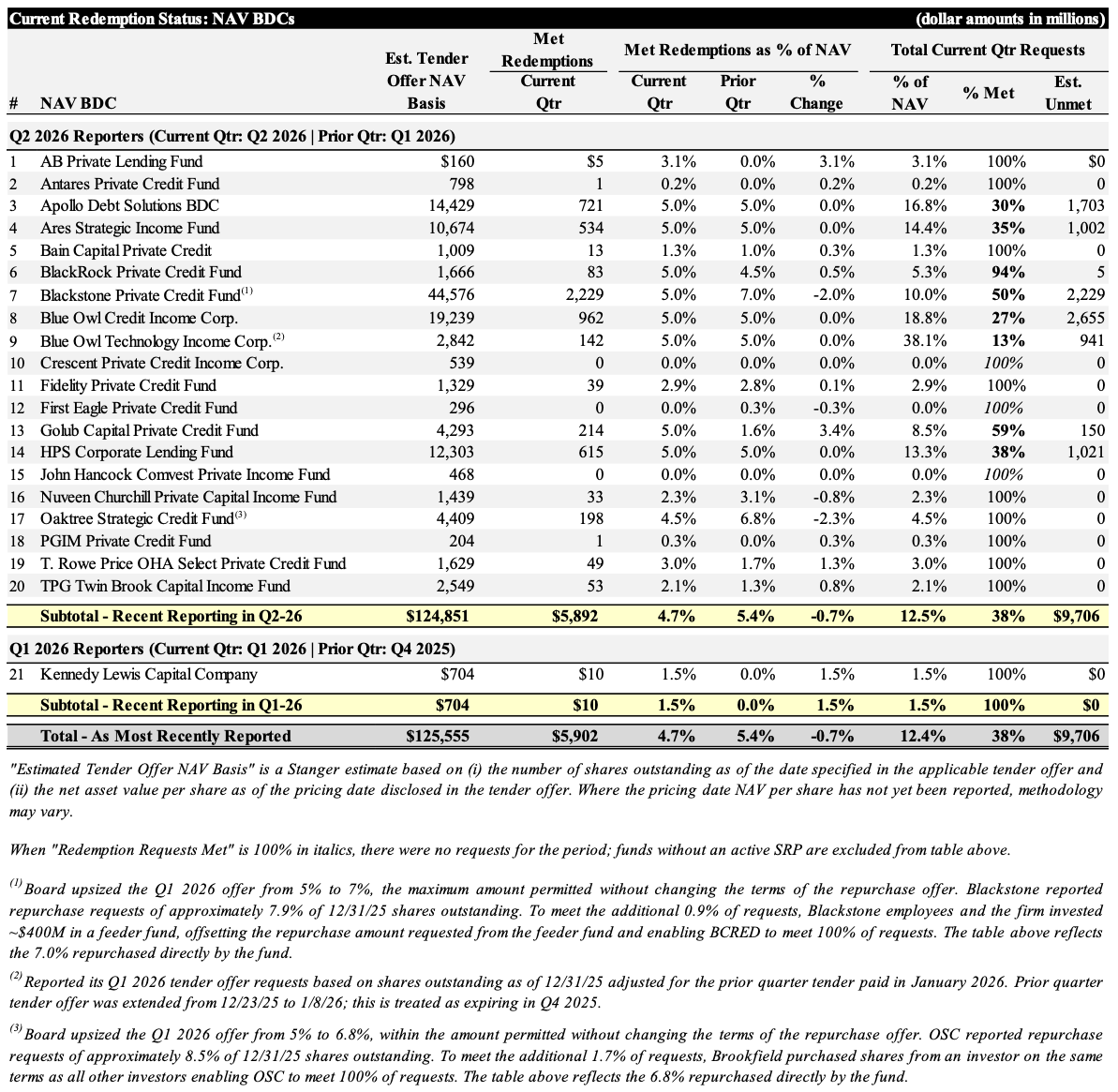

The $5.9 billion Q2 2026 total extends a rotation dynamic that has defined nontraded BDC flows for most of the year. Publicly registered nontraded BDCs saw outflows exceed inflows for the first time in the first quarter, and the pattern has held at the fund level through the second quarter – with sharply divergent outcomes. Apollo Debt Solutions BDC disclosed the largest demand of the quarter at approximately 16.8% of shares, the highest since its 2022 launch, while Ares Strategic Income Fund reported demand of 14.4% and Morgan Stanley’s North Haven Private Income Fund saw demand of 11.6%, enough to force a 43% proration. Others cleared the bar more comfortably: Oaktree Strategic Credit Fund’s Q2 tender came in at 4.5%, avoiding proration for the first time since the fourth quarter of 2025, a reversal from a first quarter that required an affiliate purchase to clear demand above the standard cap.

“While redemption requests in private credit remain elevated, sponsors are continuing to meet those requests within defined program limits,” said Kevin T. Gannon, chairman and chief executive officer of Stanger. “What we’re watching is a rotation, not a retreat, with investors rebalancing out of credit and into [hard assets with low obsolescence] strategies. The semi-liquid structure allows them to do so on defined terms, protecting the investors who want to stay without forcing distressed sales inside the fund. That’s the mechanism working exactly as intended.”

Gannon has used similar language for months to describe where the capital leaving credit is going. Stanger’s data through May showed combined nontraded BDC fundraising of approximately $11.9 billion, down 55% year-over-year, against approximately $12.9 billion in redemptions – net outflows of roughly $1 billion for the category. Over that same span, combined real estate and infrastructure fundraising, or HALO strategies, reached approximately $23.1 billion, up 33% year-over-year, with infrastructure strategies rising 61%, a figure that includes Blackstone Digital Infrastructure Trust’s (NYSE: BXDC) public listing. Credit’s share of overall alternative-investment fundraising has fallen from more than half to roughly a third, Gannon has said.

Reported Q2 2026 tender offer results for the full NAV BDC landscape are detailed in the table below.

Founded in 1978, Robert A. Stanger & Co. is an investment banking firm providing advisory, valuation, and capital markets services to real estate investment trusts, partnerships, and related entities.

Visit the AltsWire directory page.