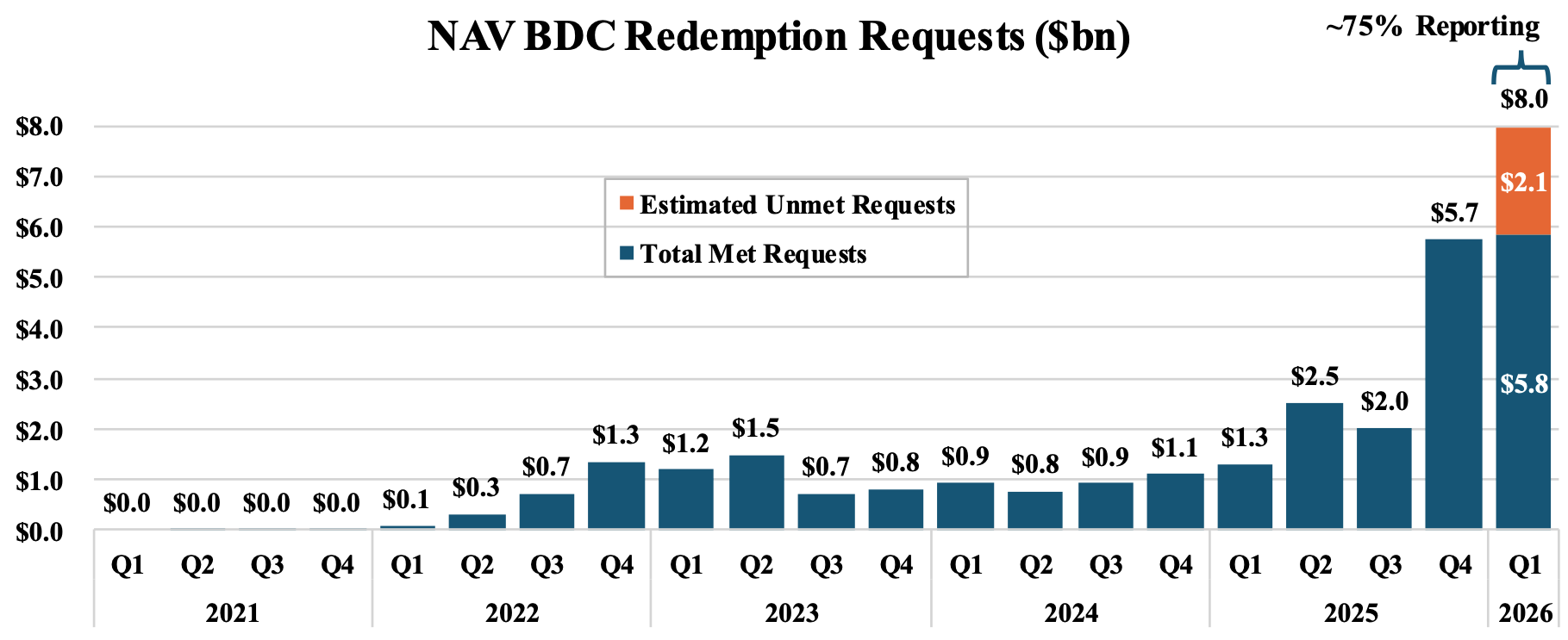

NAV BDCs Return More Than $5.8B in Q1 Liquidity as Proration Hits for First Time

Net asset value business development company sponsors have delivered more than $5.8 billion in liquidity to investors so far in the first quarter of 2026, with approximately 75% of the market reporting, according to investment banking firm Robert A. Stanger & Company Inc.

NAV BDCs are structured with a quarterly redemption cap of 5% of shares outstanding. Where redemption demand has exceeded that limit, programs have either capped redemptions at 5% and prorated payments to investors or expanded capacity to meet demand.

This structure is designed to protect investors remaining in the fund while also providing liquidity to those seeking to rebalance their portfolios.

Q1 2026 marks the first instance of proration for NAV BDCs. Stanger’s data indicate $2.1 billion in redemption requests have gone unfulfilled so far in the quarter, with several large NAV BDCs still expected to report in the coming weeks. That figure includes both Blue Owl BDCs which combined to return more than $1.5 billion to investors in Q4 2025.

Apollo Global Management said it would fulfill roughly 45% of first-quarter redemption requests in Apollo Debt Solutions BDC, and Ares Management’s BDC, Ares Strategic Income Fund, fulfilled approximately 43.1% of capital sought by shareholders in Q1 2026.

“The $5.8 billion in liquidity provided to NAV BDC investors so far in Q1 is a testament to how these vehicles are designed,” said Kevin T. Gannon, chairman and chief executive officer of Stanger. “Semi-liquid structures like NAV BDCs are built to accommodate investor redemptions within defined program limits, and that is exactly what we are seeing.”

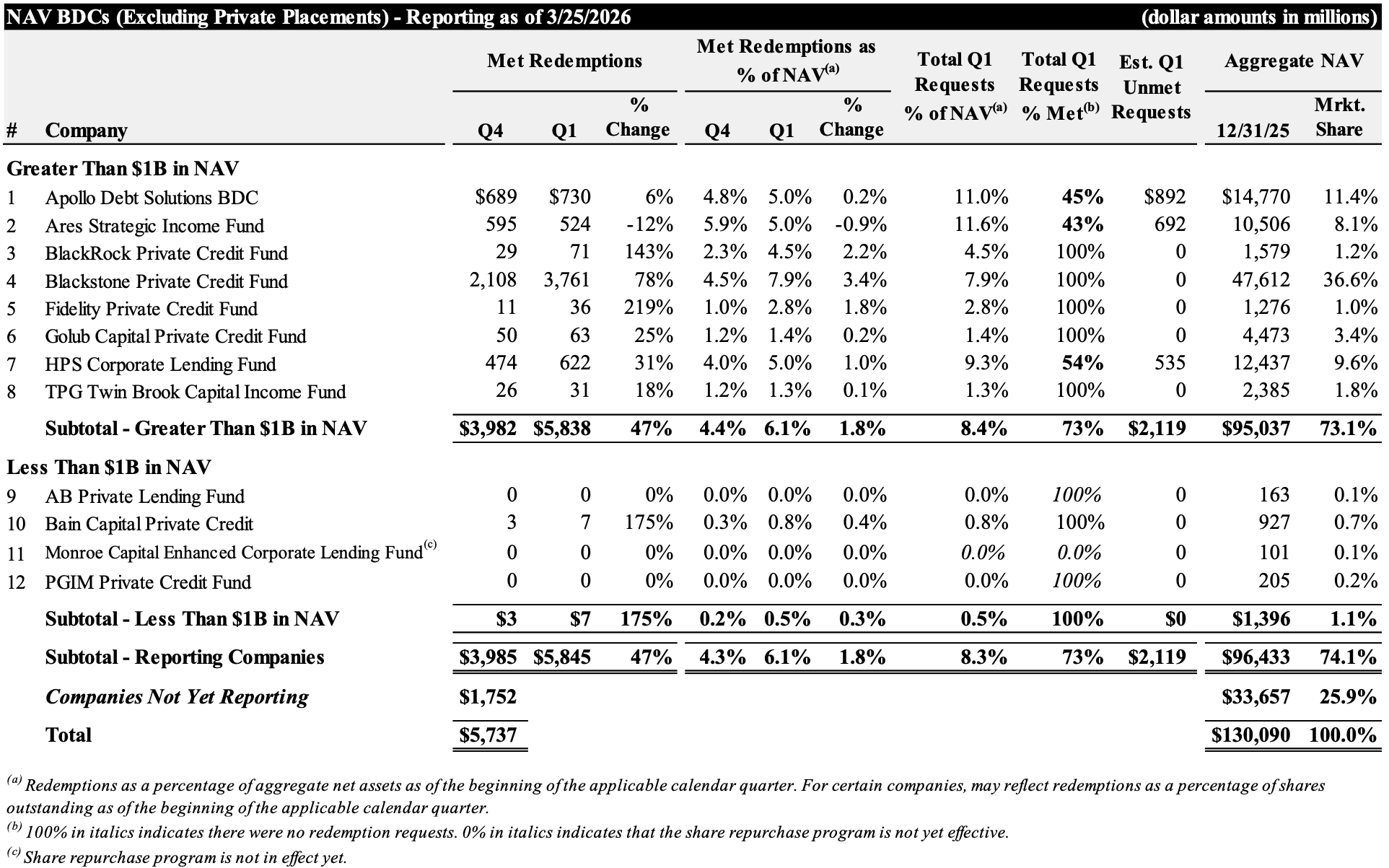

Reported Q1 2026 tender offer results for the full NAV BDC landscape are detailed in the table.

“The comparison to NAV REITs in 2022 is instructive — those vehicles navigated a similar period of elevated demand and demonstrated the efficacy of the product. The record liquidity delivered so far this quarter is the clearest evidence yet that these structures are working exactly as promised,” added Gannon.

Stanger’s Gregory R. DiSalvo, managing director, noted that the firm’s preliminary data from private placement BDCs indicate the companies are following a similar trend to their publicly registered counterparts, “a meaningful signal as we track the market’s evolution.”

Founded in 1978, Robert A. Stanger & Company is an investment banking firm providing advisory, valuation, and capital markets services to real estate investment trusts, partnerships, and related entities.

Visit the AltsWire directory page.