Sponsored: Qualified Opportunity Zone 2.0 Funds – Why Investment Vehicle Structure Matters

By Sponsored

By Nick Rosenthal, Co-Chief Executive Officer, Griffin Capital Company

EXECUTIVE SUMMARY

The Qualified Opportunity Zone 2.0 program, enacted under the One Big Beautiful Bill Act, creates one of the most powerful long-term tax planning tools available to investors: a rolling five-year deferral on invested capital gains, a 10% reduction at the end of that deferral period and, the program’s defining benefit, permanent exclusion on all appreciation and depreciation recapture for investors who hold their fund interest for at least 10 years.

The potential benefits are substantial, but they depend on timelines that create a fundamental problem for perpetual, open-end QOZ fund vehicles. Because QOZ 2.0 operates on a rolling, investor-specific tax clock, with no common deadline to align cohorts, every investor who enters a perpetual fund runs their own independent five-year and 10-year timeline. For perpetual QOZ funds, the result is a fund populated by investors who have materially different tax profiles and optimal exit windows but are all subject to the same portfolio decisions.

For advisers and wealth platforms evaluating QOZ 2.0 fund opportunities, structure should be a primary consideration as it can materially affect outcomes for their clients.

HOTEL CALIFORNIA AND THE PERPETUAL QOZ FUND TRAP

There is a famous line from the Eagles’ 1977 classic Hotel California: “You can check out any time you like, but you can never leave.” The song is about a traveler who arrives at a beautiful, welcoming hotel, lured by warm lights, pleasant company, and the promise of comfort, only to discover, too late, that the place operates by its own rules. The checkout desk exists, the paperwork is available, but when you want to leave, you discover you can’t.

It is an almost perfect analogy for the structural limitations of a perpetual QOZ fund, with one important distinction. In Hotel California, the doors are metaphorically locked. In a perpetual QOZ fund, the gates are real, and management has a limited number of options that will allow you to check out without negatively impacting other guests.

With the implementation date for the QOZ 2.0 program approaching rapidly, some investment managers are contemplating ways to structure semi-permanent capital vehicles. The appeal is logical: perpetual vehicles can be accretive to enterprise value, eliminate the need to repeatedly reconstitute a selling group, and spread vintage risk across both cycles and a larger, more diversified portfolio. However, the appeal begins to fade once you evaluate the liquidity levers available to a manager navigating materially different tax timelines across investor cohorts.

Consider the harvest. A farmer plants and tends to a crop with great skill for years, but if different rows of the field mature at different times with no mechanism to pick them separately, the farmer has no good options. How one exits should not be a secondary consideration in a QOZ fund; it is central to recognizing the primary benefit of long-term tax-free growth. The 10-year appreciation exclusion is the harvest, but a perpetual fund is a farm with no harvesting plan and no agreement among the farmers about when to pick.

Perpetual private real estate vehicles can typically create liquidity for existing investors in four ways:

- Inflows: Investors entering the vehicle replace investors exiting;

- Leverage: Generating liquidity through increased borrowings;

- Asset sales: Selling assets to create liquidity; and

- Public listings: Completely changing the structure and providing liquidity at the expense of public market volatility and pricing dynamics.

What makes each of these mechanisms problematic is the nature of real estate market dynamics in the context of the QOZ structure itself. Investors have presumably invested in the vehicle to maximize its most powerful tax benefit, tax-free growth after a 10-year holding period. As a result, most investors or their beneficiaries will likely want to redeem their interest after 10 years, with Year one investors seeking to exit after Year 11, Year two after Year 12, and so on. This dynamic creates an inherent misalignment between the various investor cohorts in a perpetual QOZ fund. With sufficient liquidity, it may be possible to manage this inherent misalignment, but the source of that liquidity may conflict directly with the tax architecture investors came for, harm remaining investors, and/or depend on market conditions that are least likely to exist when liquidity is most needed.

The reason is cohort misalignment. Under QOZ 2.0’s rolling, vintage-specific tax clock, each investor’s five-year deferral and 10-year exclusion run from the date of their own investment, with no common deadline to create even temporary alignment. A perpetual fund accumulates investors with irreconcilably different tax timelines. A Year one investor’s 10-year exclusion matures in Year 11. A Year 12 investor’s clock does not expire until Year 22. They share the same portfolio and the same fund documents. They do not share the same tax reality.

When performance or outlook softens, investors who have satisfied their 10-year holding period will want to exit. The manager cannot sell assets to fund their redemptions without allocating taxable gains to every other investor in the fund, including investors who have not reached their 10-year holding period and have no desire to exit and no interest in an unexpected tax bill. The fiduciarily rational response is to gate redemptions. And when that gate closes, it closes for everyone, even those who have surpassed their 10-year holding periods and, potentially, their beneficiaries.

This is not a management failure. It is a structural one, present from day one, compounded with every additional year of capital formation. The sections below explain why each liquidity mechanism fails in the QOZ context, and why a finite-life structure eliminates the problem at its root.

I. THE QOZ 2.0 TAX CLOCK: WHY VINTAGE ALIGNMENT IS EVERYTHING

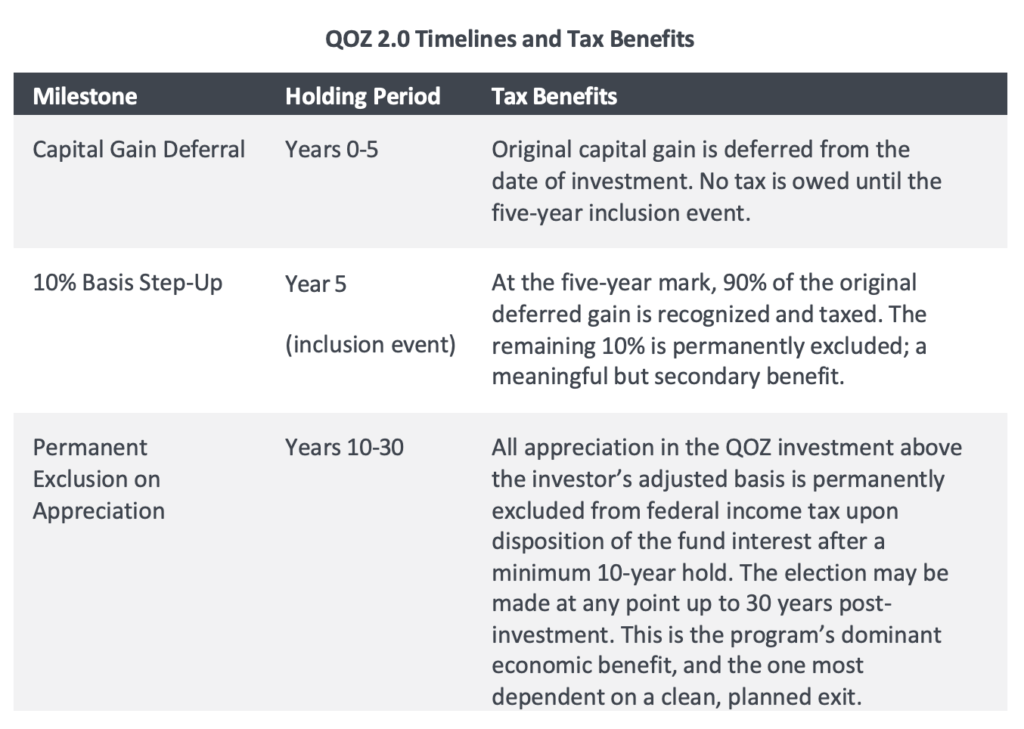

To understand why each liquidity lever fails, it helps to be precise about how the QOZ 2.0 benefits accrue. Unlike the original QOZ program, which had a fixed, mandatory gain inclusion date of Dec. 31, 2026, regardless of when an investor entered, QOZ 2.0 introduces a rolling, investor-specific benefit schedule running from the date of each investor’s qualifying investment:

Again, the ability to avoid capital gains tax on the QOZ fund investment is the largest and most significant potential benefit of the program, but it is also the one that may be at most risk in a perpetual fund structure since it requires a clean exit for investors at or after the 10-year mark.

Key Insight

QOZ 2.0’s rolling tax clock is an improvement for investors, democratizing this benefit for all investors, but it creates more disparity amongst each investor’s timeline. In a perpetual fund operating under 2.0 rules, there is no convergence event or natural moment of alignment.

II. THE FOUR LIQUIDITY LEVERS, AND WHY EACH ONE FAILS

When investors in a perpetual fund seek to exit, the portfolio manager typically has four tools it can use to provide that liquidity. However, each has a version of the same core problem: it either conflicts with the QOZ tax structure, harms remaining investors, or depends on market conditions that often do not exist when liquidity is most needed.

A. Inflows: The Lever That Stops When You Need It Most

New capital from incoming investors is the most natural source of liquidity that perpetual funds can use to pay redemptions. If inflows exceed redemption requests, then the manager may be able to satisfy those requests in a way that does not negatively impact remaining investors. This dynamic may be present if the fund is performing well and the fundraising environment is favorable, but often evaporates when it is most needed.

Capital inflows are procyclical. They are highest when a fund is performing and asset class sentiment is positive. When a fund gates redemptions due to performance or perceived future stress, new subscriptions often slow or stop entirely. Investors are reluctant to invest in a fund that was structured to allow redemptions but is no longer able to do so. As a result, there is a strong possibility that this lever will disappear as soon as it is needed most. Inflows are a liquidity source during growth, not a solution during stress.

Relying on new inflows as a liquidity mechanism requires an indefinitely growing pool of tax-motivated investors willing to deploy fresh capital into a vehicle with a redemption queue. That pool does not exist at the scale required to resolve a meaningful redemption backlog.

B. Leverage: A Short-Term Fix That Compounds the Underlying Problem

Drawing on credit facilities or seeking new financing preserves the assets in the underlying portfolio, while generating cash for redemptions. It avoids asset sales and the related tax consequences for investors. However, in a real estate fund, it can make the underlying situation worse.

Additional leverage is particularly problematic if a fund is already underperforming or facing significant redemption pressure. It increases risk and decreases future cash flows for both redemptions and distributions to investors. Though it may allow some investors to exit in the short term, remaining investor are forced to absorb the additional risk, and the impact on future cash flows may limit their ability to exit the fund in the future. There is no way to predict the cost and availability of this capital, particularly during market downturns, and it would be irresponsible to rely on it as a source of liquidity.

C. Asset Sales: The Direct Solution That the QOZ Structure Prohibits

If a conventional fund needs a significant amount of liquidity, selling assets may be the best option. However, it creates meaningful issues for investors in a QOZ fund given its structure and tax benefits.

When a fund sells an asset at a gain, the associated tax liability is borne by all investors in a diversified fund, regardless of whether or not they redeem their interests. This may not be an issue for a QOZ fund if all its investors have held their interest in the fund for at least 10 years, since they can elect to exclude the gain from their taxable income. However, this is unlikely to be the case for a perpetual QOZ fund, and there is no way to allocate the capital gain to only those investors who have met the 10-year requirement. As a result, investors who have not yet reached the 10-year mark will incur a capital gain tax liability that they may have been able to avoid if the asset had been sold later. This is in direct conflict with the biggest benefit of the structure, long-term tax-free growth.

D. Public Listings: Changing the Structure to Solve a Problem the Structure Created

Converting a perpetual QOZ fund into a publicly traded vehicle (an exchange-listed fund or REIT) is occasionally proposed as a path to investor liquidity. It addresses the symptom (i.e., liquidity for investors seeking to exit), while potentially destroying the primary reason investors entered the fund in the first place: long-term, tax-free growth.

Execution risk is substantial. A successful public listing requires favorable market conditions, SEC registration, underwriter relationships, and meaningful demand from new investors. But if a fund is already facing significant redemption pressure, it’s likely that a large swath of its investors will want to sell their shares as soon as the listing is completed, and new investors will be reluctant to step in until this selling pressure subsides. A proper balance of buyers and sellers is critical for a publicly traded vehicle. If there are more sellers than buyers, it drives the stock price down to a level that’s low enough for new investors to step in. The result is a price that may be significantly less than the intrinsic value of the portfolio and returns for investors that may be significantly less than what they would have been able to achieve if the listing did not occur.

Public listing is not a liquidity solution. It is a structural transformation that may trade one set of problems for another.

Why Liquidity Levers May Fail for a Perpetual QOZ Fund

- Inflows: Procyclical (often dry up precisely when needed); a visible gate makes raising new capital nearly impossible.

- Leverage: Increases risk and restrains cash flows to remaining investors; defers the problem while compounding it.

- Asset sales: Potentially tax-destructive to investors who have not held for 10+ years.

- Public listing: Market volatility and an imbalance between buyers and sellers may drive the stock price below net asset value.

III. WHY FINITE-LIFE STRUCTURES SOLVE THE PROBLEM AT ITS ROOT

A finite-life QOZ fund, with a clearly defined investment period and a contractually committed wind-down keyed to the 10-year exclusion threshold, does not face the cohort misalignment problem because it never creates one. There are no ad hoc redemptions to satisfy, and there is no conflict between investor cohorts with different exit timelines. The structure delivers the QOZ program’s primary benefit, the 10-year appreciation exclusion, as a contractual feature, not a managerial preference.

A. Cohort Alignment: One Clock, One Exit

A finite-life QOZ fund typically closes its subscription period after 12 months to 24 months. All investors who enter during that window run materially identical tax timelines: their five-year deferral and inclusion events cluster within a narrow band, and their 10-year exclusion milestones converge on the same approximate exit window. The portfolio manager can build the entire investment strategy (acquisition timing, debt structure, value-add scope, disposition sequencing) around a single cohort’s tax horizon, because there is only one horizon to serve. When the fund approaches wind-down, the manager executes a deliberate disposition process knowing that timing serves the tax interests of virtually every investor in the fund simultaneously.

B. Contractual Exit: A Right, not a Preference

The most important distinction between a finite-life and a perpetual fund is not economic; it is a matter of investor rights. In a perpetual fund, investors who have reached their 10-year exclusion threshold typically have limited legal mechanisms, if any, to demand a wind-down when redemptions aren’t available. They have earned a tax benefit they probably cannot access without the manager’s cooperation, and the manager may not have a contractual obligation to provide it on any particular timeline.

In a finite-life fund, the wind-down is a legal commitment, often with investor voting rights attached to any potential extension. The manager usually has a fiduciary and contractual obligation to liquidate the portfolio and return capital within the fund’s defined term. Investors know this before they subscribe. The exit is a structural feature of the investment.

C. Manager Alignment: Compensation and Investor Outcomes

In a perpetual fund, the manager’s economics favor continuing the fund and retaining capital. Management fees accrue on the fund’s assets under management for as long as the fund operates. A wind-down eliminates that fee stream. A manager who is not contractually required to liquidate has a latent financial incentive to defer disposition, continue raising capital, and maintain the fund indefinitely, regardless of whether continued operation serves investor interests.

Managers of perpetual funds also typically earn incentive fees to the extent a fund’s performance in a given year exceeds a minimum return threshold. The minimum return is based on both realized and unrealized returns for investors and, therefore, is largely based on the estimated value of the fund, which may or may not be determined by an independent third party. They are not contingent upon investors being able to liquidate their investment, so the manager may earn an incentive fee even though investors haven’t fully realized the return upon which it was based.

In a finite-life fund, the manager earns asset management fees over a specified period of time, and incentive fees are usually only realized at wind-down, subject to performance hurdles. There is no inherent conflict of interest relative to management fees and redemptions, and incentive fees are not earned until investors actually receive distributions that exceed their original investment and the minimum return threshold. This is the alignment structure that institutional investors have long demanded in private fund contexts, and it is particularly suited to QOZ investment given the long holding period and the primary tax benefit’s dependence on a clean, contractually committed exit.

D. Portfolio Discipline: Built Around the Harvest

A finite-life fund’s defined exit horizon imposes discipline on every element of portfolio construction. Assets are acquired and debt is structured with a specific disposition timeline in mind. Development and value-add programs are scoped to deliver exit-ready assets within the operational timeline. The manager maintains a disposition schedule as the fund approaches its term, not as a reactive response to investor pressure, but as a planned feature of fund operations that was embedded in the underwriting from the first acquisition.

The harvest is not an afterthought. It is predefined, providing better transparency and clearer expectations for investors.

Key Insight

A finite-life QOZ fund does not simply avoid the liquidity problems associated with redemptions; it makes them structurally irrelevant. There are no misaligned cohorts to manage and no mid-cycle asset sales that harm certain investors. The structure delivers what the QOZ program was designed to provide: a long-term, disciplined, tax-advantaged investment, with a clear contractual path to an investor timeline they understood before they ever subscribed.

III. CONCLUSION: YOU SHOULD BE ABLE TO CHECK OUT

The Eagles’ Hotel California does not end with the narrator choosing to stay. It ends with him discovering he was never really free to leave. There is a reasonable probability that a perpetual QOZ fund investor suffers the same fate. Investors do not make an informed decision to remain when the gate closes. They are told that departure is not available because the structure they invested in was designed without regard for managing the nuances of tax dynamics inherent in creating liquidity for QOZ investors.

For investors and advisers evaluating QOZ 2.0 fund opportunities, structure is not a secondary consideration. It is the primary one. A well-managed perpetual fund is still a perpetual fund and the structural liabilities described in this paper do not disappear with capable management. They wait for the conditions that will eventually expose them. When those conditions arrive, the hotel doors will be closed, potentially for a very long time.

Nick Rosenthal serves as co-chief executive officer at Griffin Capital Company, where he is responsible for working directly with the firm’s executives across acquisitions, asset management, due diligence, product development, accounting, investor relations, marketing and equity sales. In this capacity, Rosenthal directs the firm’s strategic vision and advances key initiatives across the organization.

Nick Rosenthal serves as co-chief executive officer at Griffin Capital Company, where he is responsible for working directly with the firm’s executives across acquisitions, asset management, due diligence, product development, accounting, investor relations, marketing and equity sales. In this capacity, Rosenthal directs the firm’s strategic vision and advances key initiatives across the organization.

This white paper is prepared by Griffin Capital Company for informational and educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security. References to QOZ 2.0 legislation reflect the One Big Beautiful Bill Act framework; investors should consult their own tax and legal advisers before making investment decisions. Tax treatment of Qualified Opportunity Zone investments is complex and subject to change. Hypothetical examples are illustrative only and do not represent the performance of any actual fund. Past performance is not indicative of future results.

Griffin Capital Company is a sponsor of AltsWire, and the article was published as part of their standard directory sponsorship package.

For more Griffin Capital Company news, visit its directory page.