Morningstar Reports Second Round of Mostly ‘Neutral’ Semiliquid Ratings

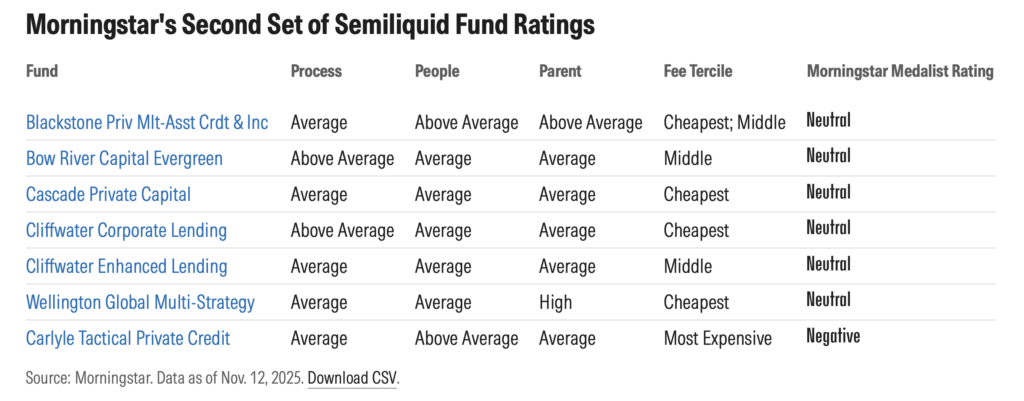

Morningstar Inc. — a leading global provider of independent investment research best known for its widely followed mutual fund and ETF ratings – has completed another round of its Morningstar Medalist Ratings for semiliquid funds from providers like Blackstone, Carlyle, and Cliffwater, but did not award any fund a “bronze,” “silver,” or “gold” rating.

These higher ratings signify a conviction that the fund can deliver superior returns over a full market cycle. Instead, analysts issued six “neutral” ratings and one “negative” rating, citing the asset class’s youth, high fees, and valuation challenges.

The ratings highlight several obstacles for this emerging asset class:

- Youth and lack of testing: The semiliquid fund universe is relatively young and untested. Many private credit funds in this class did not exist during the last major credit spread blowout in early 2020, and none predate June 2018. Indeed, Blackstone Private Multi-Asset Credit & Income Fund and Wellington Global Multi-Strategy Fund – the newest of the bunch – launched in 2025 and 2024, respectively.

- Opaque valuations: Different valuation practices make it difficult for investors to pin down risks. For example, some private equity funds were in the black in 2022 despite the Morningstar U.S. Market Index dropping 18%. Additionally, funds in the same asset class can show divergent returns, illustrating how different pricing approaches affect performance (e.g., Carlyle Tactical Private Credit Fund lost 17% in 2020 versus Cliffwater Corporate Lending Fund’s 4% decline).

- High fees: Fees are a clear hindrance and a strong predictor of future success. The average adjusted fee eclipsed 3%, which is significantly higher than the approximately 1% average for actively managed mutual funds and ETFs. This steep cost sets a high bar for funds to beat their peers over the long term.

- Complexity: The funds are complex not only in their portfolios but also in their fee structures, which often include performance fees with catch-up provisions that can function like an additional management fee.

Despite drawbacks, Morningstar analysts said they were impressed with Blackstone’s and Carlyle’s portfolio management teams and Bow River Capital Evergreen Fund’s and Cliffwater Direct Lending Fund’s investment processes.

Morningstar plans to release more semiliquid fund ratings in 2026, which will include tender-offer funds, non-traded business development companies, and non-traded real estate investment trusts. According to the company, the ratings are selected based on investment merit and investor demand to help investors and advisers sort through the growing number of choices in this asset class.

First Trust Alternative Opportunities Fund was among the first group of semiliquid funds to be rated in September and received a “negative” rating. The accompanying analyst commentary indicated that the lowest rating was influenced by structural concerns.

Morningstar is a global provider of independent investment insights offering an extensive line of products and services for individual investors, financial advisers, asset managers and owners, retirement plan providers and sponsors, and institutional investors in the debt and private capital markets.

Click here to visit the AltsWire directory page.