Monroe Capital Registers $1 Billion BDC to Target Lower Middle-Market Lending

Chicago-headquartered asset management firm Monroe Capital LLC has registered a new non-traded business development company with the U.S. Securities and Exchange Commission. Monroe Capital Enhanced Corporate Lending Fund, or M-LEND, seeks to raise up to $1 billion in common shares of beneficial interest.

The BDC election remains pending SEC effectiveness, but M-LEND has articulated a clear focus on directly originated and proprietary lending to the U.S. lower middle market.

Providing capital solutions within the United States and Canada since 2004, Monroe Capital specializes in private credit markets across various strategies, including direct lending, asset-based lending, specialty finance, alternative credit solutions, structured credit, venture debt, and equity. The firm reported $21.6 billion in committed and managed assets under management as of July 1, 2025.

M-LEND’s primary objective will be to originate and invest primarily in senior secured loans, as well as club transactions – loans arranged by smaller lender groups – and syndicated loans offered to multiple lenders.

Under normal circumstances, the fund seeks to invest at least 80% of total assets (net assets plus borrowings for investment purposes) in credit and credit-related instruments issued by corporate issuers. Eligible credit instruments include notes, bills, debentures, bank loans, and convertible or preferred securities. A smaller portion of the fund’s investments may be comprised of what it calls “covenant-lite loans,” referring to loans that do not have a complete set of financial maintenance covenants.

The fund defines its target borrowers, U.S. lower middle-market companies, as those generally possessing annual revenue between $50 million and $350 million, annual earnings before interest, taxes, depreciation, and amortization between $3 million and $35 million, and annual recurring revenue between $50 million and $250 million. The BDC may also selectively invest in foreign instruments and illiquid and restricted securities.

Upon effectiveness, M-LEND will be externally managed by Monroe Capital BDC Advisors, LLC. The fund also intends to elect to be treated as a regulated investment company for federal income tax purposes.

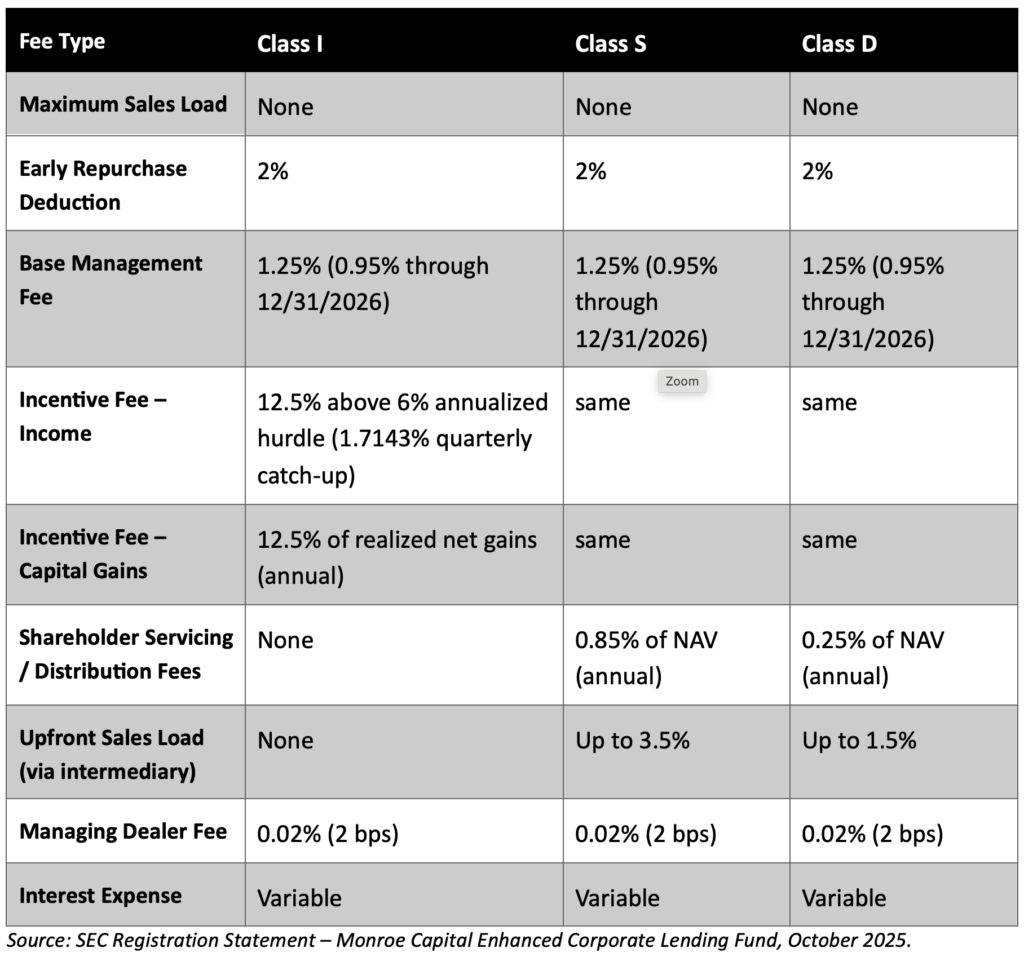

The offering will include three separate share classes – Class S, Class D, and Class I – to accommodate different investment platforms and fee structures. The minimum initial investment for Class S and D shares is $2,500, and the minimum for Class I shares (unless waived by the fund or managing dealer) is $1 million. The company intends to pay regular monthly distributions.

Share Class Breakdown

Class I Shares – Designed for institutional and advisory platform investors, such as registered investment advisors (RIAs), family offices, and qualified institutional buyers accessing the fund through fee-based programs. Class I carries no sales load or servicing fees, making it the lowest-cost share class.

Class D Shares – Geared toward brokerage and advisory clients accessing the fund through broker-dealer or hybrid advisory platforms that charge a modest servicing fee. Class D includes a 0.25% annual distribution and servicing fee, with no upfront sales load, and typically suits investors working through low-commission or advisory channels.

Class S Shares – Intended for retail investors purchasing through traditional brokerage channels. This class includes an ongoing 0.85% servicing fee and may be subject to up to a 3.5% upfront placement fee from intermediaries. It is designed to compensate selling brokers for distribution and shareholder servicing.

The purchase price for each share class will be equal to the fund’s net asset value per share, calculated as of the day preceding the monthly share purchase. M-LEND has already secured an exemptive order from the SEC, which permits it to issue these multiple share classes with varying shareholder servicing and distribution fees.

Fee Breakdown by Share Class

Each class is subject to different fees and expenses.

Management fee: The adviser will be paid an annual management fee of 1.25% of the fund’s average total assets (which includes assets financed using leverage). No management fee will be charged on the portion of the fund’s total assets below a 200% asset-coverage ratio. Through December 31, 2026, the adviser has voluntarily agreed to waive a portion of this fee, reducing it to 0.95% of average total assets.

Incentive fee: The incentive fee consists of two components:

- Income incentive fee: 12.5% of the pre-incentive fee net investment income for each calendar quarter, subject to a 6.0% annualized hurdle rate, with a catch-up to 1.7143% per quarter and 12.5% thereafter.

- Capital gains incentive fee: 12.5% of cumulative realized capital gains, net of realized losses and unrealized depreciation, paid annually in arrears.

Distribution and servicing fees:

Class S: 0.85% of NAV (annual)

Class D: 0.25% of NAV (annual)

Class I: None

All are paid monthly in arrears.

Upfront sales load: None charged by the fund; however, intermediaries may charge up to 3.5% (Class S) or 1.5% (Class D) directly to investors.

Managing dealer fee: The fund pays a 0.02% (2 bps) fee on capital raised to its managing dealer, InspereX LLC.

Leverage / interest expense: Variable and dependent on borrowing costs; not a fixed percentage.

Fee Summary by Share Class

The offering is being conducted on a “best efforts” basis by the managing dealer, InspereX LLC, meaning the firm is not obligated to sell a specific amount of shares. Furthermore, for its Class S and Class D shares, M-LEND intends to hold investor funds in escrow until purchase orders are received from at least 100 investors for each respective class.

The registration of M-LEND underscores continued momentum in the non-traded BDC market, as managers seek to expand access to private credit through perpetual vehicles. Monroe’s focus on lower middle-market borrowers reflects a broader industry trend toward smaller, relationship-driven lending as banks retreat from this segment.

Click here to visit the AltsWire directory page.