Emerging BDC Redemption Trends Echo Earlier Non-Traded REIT Liquidity Cycle

Redemption activity is beginning to surface in the non-traded business development company market after several years of rapid fundraising growth, raising questions about whether the sector may follow the liquidity cycle that reshaped non-traded real estate investment trusts beginning in 2022.

A new analysis from Robert A. Stanger & Company examines the emerging redemption dynamics and compares them with the earlier REIT cycle.

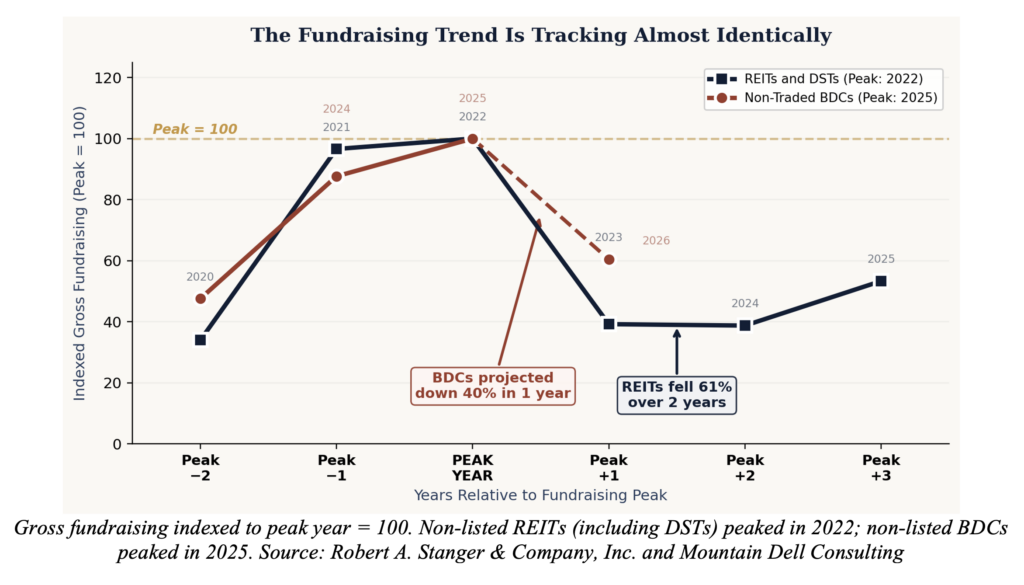

The comparison highlights a pattern familiar to many market participants: declining fundraising followed by rising redemption requests. This sequence has reshaped the non-traded REIT market over the past several years, and early data suggests the non-traded BDC sector may be entering the early stages of a similar liquidity cycle.

The BDC market remains stable for now, as no non-traded BDC has any unmet redemption requests, despite several funds, most recently Blackstone Private Credit Fund, or BCRED, exceeding their standard 5% quarterly repurchase provisions. Still, declining inflows and rising redemption activity are beginning to mirror the early stages of the non-traded REIT cycle.

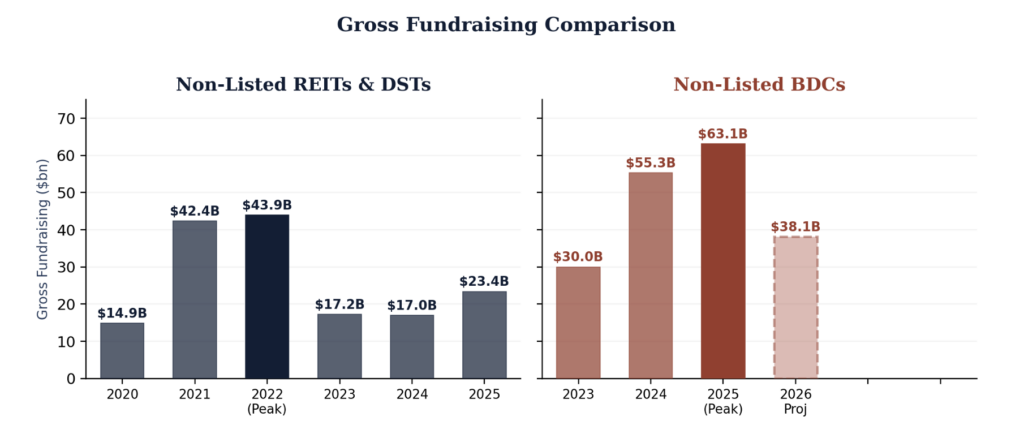

Non-traded BDCs experienced a period of extraordinary growth during the expansion of private credit markets. Driven by rising interest rates and strong demand for credit strategies, the sector grew from $3.5 billion of capital formation in 2020 to $63.1 billion in 2025, making it one of the fastest-growing segments of the alternative investment market.

However, as Stanger reported, BDC fundraising momentum has slowed in recent months, down nearly 50% from its early 2025 high. When indexed to its peak year and compared with the earlier REIT cycle, the trajectories begin to look strikingly similar.

The decline itself is not unusual in cyclical markets. What followed historically is more instructive. In the non-traded REIT market, redemption pressure persisted for several quarters after fundraising began to slow. Although redemption pressure began to normalize in mid-2024, fundraising levels have yet to recover to their 2021 to 2022 highs.

The decline itself is not unusual in cyclical markets. What followed historically is more instructive. In the non-traded REIT market, redemption pressure persisted for several quarters after fundraising began to slow. Although redemption pressure began to normalize in mid-2024, fundraising levels have yet to recover to their 2021 to 2022 highs.

Redemption Activity Is Now Emerging

Recent disclosures suggest the BDC market has entered this phase of the cycle.

BCRED, the largest non-traded BDC, reported redemption requests of approximately 7.9% of net asset value in Q1 2026. Fulfilling all requests required the repurchase limit to be increased from 5% to 7%, along with an additional $400 million investment from Blackstone and its employees.

The next four largest funds fully satisfied Q4 2025 redemption requests ranging from 4% to 6%, while Blue Owl Technology Income Corp. repurchased more than 15% after increasing its original offer from 5% to approximately 19%.

In the short term, these levels remain manageable. The more important question is whether redemption activity continues to rise.

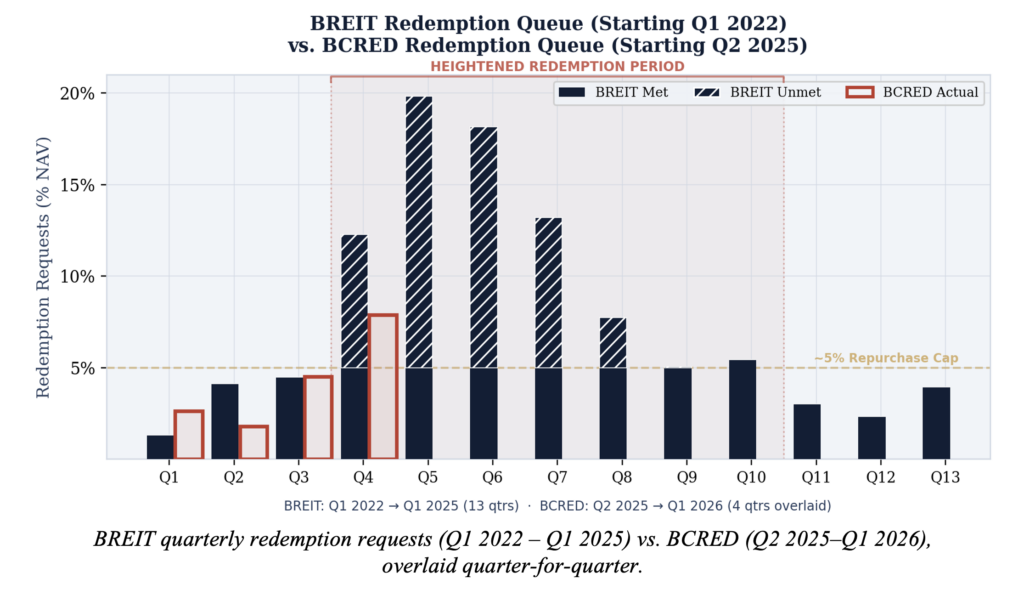

When BCRED’s Q1 2026 redemption data is compared with Blackstone Real Estate Income Trust’s, or BREIT’s, redemption cycle on a quarter-for-quarter basis, the early trajectories also appear similar.

BREIT quarterly redemption requests (Q1 2022 to Q1 2025) vs. BCRED (Q2 2025 to Q1 2026), overlaid quarter-for-quarter. Source: Robert A. Stanger & Company Inc.

BREIT’s first quarter of elevated redemption requests was approximately 12% of NAV and peaked in the following quarter at just under 20% of NAV. Elevated redemption requests persisted for another six quarters before falling back below the repurchase limits. BCRED currently stands at 7.9% of NAV in Q1 2026.

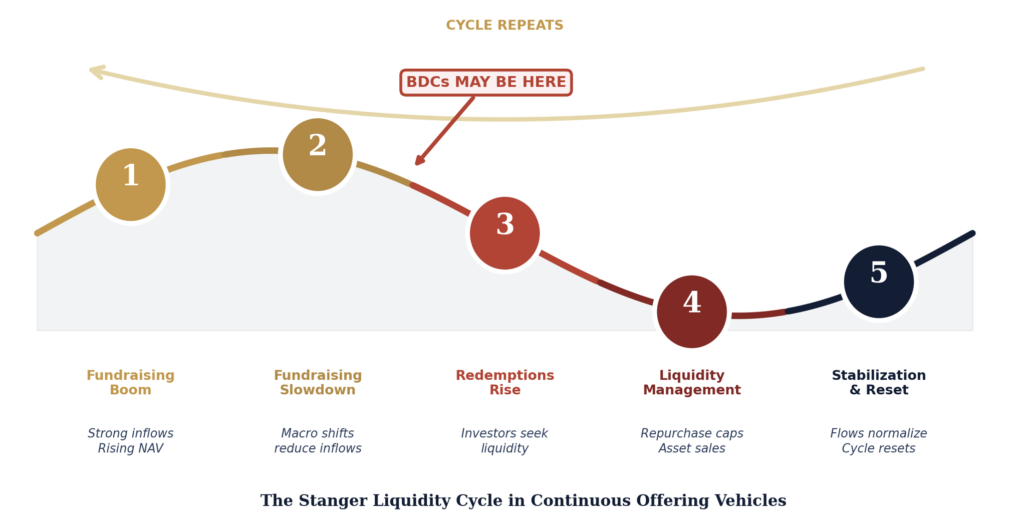

“We have been tracking capital flows in non-listed alternatives for nearly five decades, and the sequence that typically drives these cycles is very consistent,” said Kevin T. Gannon, chairman and chief executive officer of Stanger. “Fundraising slows first. Redemption requests begin to rise over the following quarters. Eventually leadership must begin managing liquidity more proactively. … I expect we will be hearing from sponsors seeking capital solutions as these dynamics unfold.”

Source: Robert A. Stanger & Company Inc.

The Central Question

The BDC market differs from non-traded REITs in several important respects. Private credit portfolios generally feature shorter-duration assets and more liquid loan secondary markets. As a result, sponsors may be better positioned to manage redemption pressure than real estate vehicles were during the REIT redemption cycle.

However, the underlying mechanics of the market remain similar. Continuous offerings funded by retail investors, combined with repurchase programs that contain quarterly limits, create a structure that functions efficiently during periods of capital inflows but can face pressure when flows reverse. The REIT and DST cycle demonstrated how quickly investor sentiment can shift once redemption requests begin to accelerate.

“Whether the BDC sector ultimately follows the same trajectory as non-listed REITs should become clearer over the coming months, as only four NAV BDCs have reported Q1 2026 tender offer results. Based on historical precedent, we expect the remaining funds to report their results between early April and mid-May,” added Michael Covello, executive managing director at Stanger.

Founded in 1978, Robert A. Stanger & Company is an investment banking firm specializing in providing investment banking, financial advisory, fairness opinion and asset and securities valuation services to partnerships, real estate investment trusts, and real estate advisory and management companies in support of strategic planning and execution, capital formation and financings, mergers, acquisitions, reorganizations, and consolidations.

Click here to visit the AltsWire directory page.