Commercial Real Estate’s Core Challenge Is a Capital Reset, Not a Broad Demand Collapse

By Greg Friedman, Managing Principal and Chief Executive Officer, Peachtree Group

Commercial real estate’s core issue is not broad-based demand destruction or short-term disruption. While office is working through its own structural demand reset, much of the broader market is navigating a capital reset, yet the industry still analyzes today’s environment using a playbook built for the appreciation cycle that followed the Global Financial Crisis.

The investment environment that produced outsized returns from roughly 2010 through 2022 was built on conditions that rarely align for extended periods. Capital was abundant, interest rates remained historically low, supply growth stayed relatively constrained across many sectors and demographic trends supported demand.

Those forces produced strong operating performance, but they also created a powerful appreciation cycle as falling costs of capital and cap rate compression expanded asset values across much of the market.

The prior cycle was supported by extraordinary liquidity conditions. Following the Global Financial Crisis, short-term rates effectively moved to zero while quantitative easing expanded the Federal Reserve’s balance sheet and increased liquidity across financial markets. That capital flowed into return-seeking assets, including commercial real estate, supporting cap rate compression and higher valuations.

The industry experienced real operating improvements, yet it also benefited from a duration-driven environment in which falling capital costs and declining discount rates amplified returns. In many cases, appreciation outpaced underlying income growth.

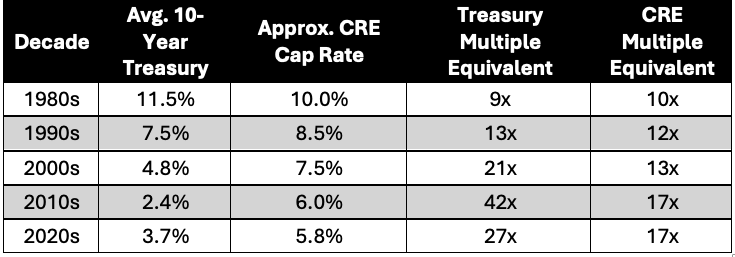

History shows how unusual that environment ultimately became.

U.S. 10-Year Treasury Yields vs. CRE Cap Rates by Decade*

*The analysis in the table uses the 10-year Treasury yields sourced from Federal Reserve historical data alongside blended commercial real estate cap rate estimates derived from institutional property market data. Cap rates reflect approximate going-in yields for stabilized institutional-quality assets and will vary by property type, geography and market conditions. Treasury and commercial real estate “multiples” are calculated as the inverse of their respective yields or cap rates, representing the implied price paid for each dollar of annual income, similar to price-to-earnings ratios in public equities. Higher multiples generally indicate more expensive pricing relative to underlying income.

The current environment is often viewed as unusual because it follows one of the strongest appreciation cycles in modern commercial real estate history. The stronger argument may be that the post Global Financial Crisis period was the anomaly as extraordinary liquidity, near zero rates, and sustained cap rate compression created an environment where appreciation frequently outpaced underlying income growth. Real estate benefited from operating improvement, but it also benefited from a duration tailwind that shifted part of the return profile from execution toward market appreciation.

That cycle has largely ended, which helps explain why today’s market feels uncomfortable despite fundamentals that remain stronger than headlines often suggest. Demand has generally held up across several property sectors, supply remains constrained, and operating performance in large parts of commercial real estate continues to be sound. At the same time, transaction activity remains uneven and refinancing pressure continues to build.

The disconnect exists because many assets remain fundamentally sound while the capital structures surrounding them do not. A hotel may be producing a healthy cash flow while carrying debt originated in a materially different interest rate environment. A multifamily project may lease successfully and still require recapitalization because construction costs moved faster than underwriting assumptions. Development projects with attractive fundamentals can stall when liquidity disappears midway through execution. These situations are not always distressed in the traditional sense; more often, they represent viable real estate attached to impaired financing structures.

That distinction matters because it changes where opportunity exists. Many of the opportunities entering the market today are less about buying broken assets and more about solving capital friction.

Assets still require repositioning and capital structures still need to be reworked. Many special situations emerge when capital dislocation moves faster than asset deterioration, creating opportunities through recapitalizations, loan acquisitions and transitional ownership arrangements even when the underlying real estate remains fundamentally sound.

This shift also changes the source of returns. During the prior cycle, markets frequently rewarded participation because abundant liquidity and declining rates supported appreciation across a wide range of assets. Strong assets performed well, but average assets appreciated too because declining rates and abundant capital supported valuations broadly. The next phase may depend less on market appreciation and more on disciplined entry points, replacement cost, operational execution, and the ability to solve complexity.

That is why the opportunity increasingly appears to be shifting from momentum-driven investing toward basis-driven investing within a broader set of special situations. The source of returns becomes less tied to market appreciation and more tied to execution. Investors who can move across credit, equity and development strategies may be better positioned because returns increasingly come from basis and execution rather than appreciation.

Commercial real estate has moved through periods like this before. Historically, some of the strongest opportunities emerged when capital became selective, markets repriced risk and execution mattered more than appreciation. Investors capable of restructuring capital, repositioning assets and establishing attractive basis often produce differentiated outcomes.

The market may be entering another version of that environment. The prior cycle rewarded appreciation. The next cycle may reward basis investing.

The opportunity now is less about waiting for valuation expansion to return and more about creating value where capital and asset fundamentals have become disconnected. That may involve repositioning assets, restructuring ownership, resetting basis, or stepping into situations where liquidity has retreated faster than demand.

The industry is not moving through a collapse. It is moving through a capital reset, and history suggests those periods often reward investors who can create value rather than wait for it.

Since co-founding Peachtree Group in 2007, Greg Friedman has overseen investments exceeding $11 billion in commercial real estate and various other enterprises. He brings extensive experience in credit and equity investing, particularly in hotels and other commercial real estate assets. Previously, Friedman served as senior vice president of business development for Specialty Finance Group, where he originated more than $2 billion of credit transactions.

The views and opinions expressed in the preceding article are those of the author and do not necessarily reflect the views of AltsWire.

For more Peachtree Group news, please visit their directory page.